Savers' Curse: Low Savings Rates and Liquid Mutual Fund Returns

(Updates with new information as of 31Jan2023, 30Sep22, 30Jun22, 30Apr22 and 31Jan22 are available at the end of this article)

Globally, savers have been getting a raw deal in the hands of central banks and governments. Even though inflation across the major nations has been running very high, central banks in these nations have been keeping interest rates ultra low, jeopardising the interests of savers.

Since the advent of petrodollars and sovereign wealth funds in the 1970s, savings glut has been bedeviling the global economy for decades. Major developed nations currently have either zero interest rates or negative interest rates, like in Switzerland, Denmark and Japan.

The ultra-low interest rates have been artificially inflating the prices of risky assets (like, stocks, commodities, crypto assets and real estate) is a different issue. A narrow set of investors who have exposure to such risky assets have benefited immensely in the past few decades.

-------------------

Read more:

Indian Mutual Funds and The Art of Ripping Off Investors

India Second Quarter GDP

Global bond yields and Interest rates

Do Paint Stocks and Crude Oil Tango?

BSE Broad and Sectoral Indices Returns

Real Estate Stocks and REITs

When Will Federal Reserve Raise Interest Rates?

Weblinks and Investing

-------------------

As argued by former Federal Reserve chair Alan Greenspan (note 1), the excess in savings is a result of globalisation, technology driving prices lower and ultra-loose monetary policies of major central banks.

It's no wonder people have been currently experiencing negative real interest rates (nominal rates adjusted for inflation) the world over. Twentieth century's great economist John Maynard Keynes described inflation and economic instability as the enemies of civilisation. Unfortunately, nobody seems to be in a mood to recall his wise words.

India is no exception to these forces. A major shift in India's interest rate policy occurred at the turn of the twenty-first century when the then Vajpayee government started reducing interest rates drastically taking advantage of low inflation--ultimately stimulating the investment demand in the country between 2003 and 2008.

Now, India is in a kind of a quandary as far as interest rates are concerned. India's central bank, the Reserve Bank of India, has been maintaining a benign interest rate policy ever since Mr Shaktikanta Das took over as RBI governor in December 2018.

India's benchmark inflation, consumer price inflation (CPI) has been running very high since of end of 2019. The COVID-19 outbreak in March 2020 complicated matters for the RBI. It was forced to cut interest rates in order to revive the economy struck by the Pandemic and the self-infected draconian nation-wide lockdowns between March and July 2020.

Even as CPI inflation has been running above the comfort zone of 5 to 6 per cent (see chart 3 below), RBI has been maintaining its low interest rate policy to stimulate the economy. Recent data suggest many of the macro indicators seem to be giving healthy signs of recovery.

The low interest rates combined with negative real yields have eroded the purchasing power of savers, especially impacting retired people and those in lower strata. That the government has kept the small savings interest rates (Post Office schemes) unchanged is a small relief.

Even the market-related instruments, like, liquid mutual funds have failed to provide any relief to market-savvy investors. During 2013 and 2014, they used to offer 9 per cent return annually--and their returns have progressively decreased to 8 per cent by 2015, 6 per cent by 2019 and to a shockingly low of 4 per cent last year (chart 1 below).

The past one-year return for liquid mutual fund is just 3.2 per cent! (Mind you, actual inflation suffered by Indians is north of 6 to 7 per cent -- official inflation data are largely fudged).

As Chart 2 below reveals,the monthly returns provided by liquid funds improved to 0.30 per cent (not annualised) from 0.25 per cent a few months ago. This is mainly due to the fact that the Treasury bill rates have improved in recent months with the 364-day Treasury bill yield moving above 4 per cent lately.

However, this is no consolation for the saving community.

Chart 2: Liquid mutual funds returns (monthly returns - not annualised):

Chart 3: Negative real interest rates (repo rate minus inflation) >

Summing Up

Savers in India have suffered for too long a time. There are not many safer instruments that protect against runaway inflation. The low interest rates have been forcing some people to dabble in outright speculation which may not be healthy in the long run.

It's time the Indian government and the RBI recognised the savers' curse and took important measures to alleviate the concerns of savers.

- - -

Additional data:

Update 23Feb2023: Liquid mutual fund returns: Data from Feb2022 to Jan2023 >

Value Research data link

As RBI has been raising its policy repo rate, short term interest rates have spiked up reflecting in the improvement in liquid mutual fund returns. As on 22Feb2023, one-year liquid returns are fetching around 5.32 percent (direct plans).

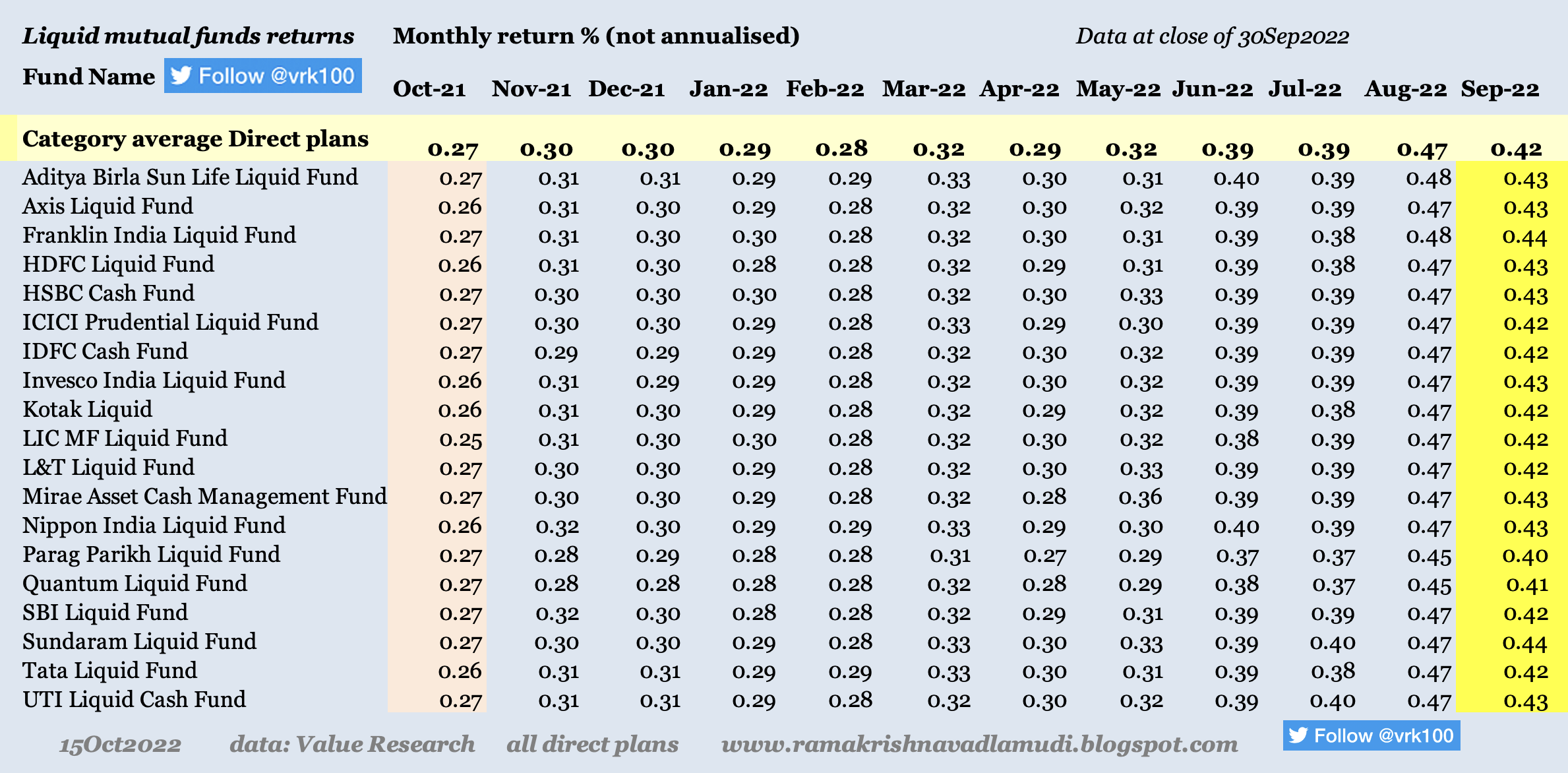

Update 15Oct2022: Liquid mutual fund returns: Data from Oct2021 to Sep2022 >

Value Research data link

As short term interest rates (like call money rate, Treasury Bill rates, etc.) have shot up in the economy in the past three to six months, there is an improvement in liquid mutual fund returns now. One-year liquid fund return fetched 3.20 percent back in Dec2021 and now they are quoting at around 4.10 percent (direct plans of liquid funds).

But the liquid fund returns are much lower than 364-day Treasury Bill rate, which is around 7.00 percent a few days back and current call money rates of 6.15 percent. Even bank fixed deposit interest rates have improved in recent months.

Update 14Jul2022: Liquid mutual fund returns: Data from Jul2021 to Jun2022 >

There is a sharp spike in liquid MF returns in the month of June 2022 to 0.39 percent from 0.32 percent in May2022, driven by rising interest rates in India >

Update 19May2022: Liquid mutual fund returns: Data from May2021 to Apr2022 >

Update 01Feb2022: Liquid mutual fund returns: Data from Feb2021 to Jan2022 >

References:

Note 1: "The Age of Turbulence: Adventures in a New World" By Alan Greenspan

Scribd Sovereign Wealth Funds 25Oct2007

Value Research liquid mutual funds returns

my tweet 05Jun2021 liquid funds

my tweet 04Feb2021 liquid funds

- - -

Disclosure: I've vested interested in Indian stocks and other investments. It's safe to assume I've interest in the financial products discussed, if any.Disclaimer: The analysis and opinion provided here are only for information purposes and should not be construed as investment advice. Investors should consult their own financial advisers before making any investments. The author is a CFA Charterholder with a vested interest in financial markets.

CFA Charter credentials - CFA Member Profile

CFA Badge

He blogs at:

https://ramakrishnavadlamudi.blogspot.com/

Twitter @vrk100