Update - Bank Disintermediation and Flow of Resources to Commercial Sector

This is an update of my article 'Bank Disintermediation and Flow of Resources to Private Sector' dated 26Sep2020:

The corporate sector and households in India raise resources from a variety of sources. Due to bank disintermediation, the commercial sector in India has got a slew of sources to raise monies from.

The commercial sector has diversified its sources of finance to non-banking finance companies (NBFCs), stock market, rights issues, private placement and foreign sources like external commercial borrowings (ECBs) and foreign direct investment (FDI).

-------------------

Read more:

India Second Quarter GDP

Global bond yields and Interest rates

Do Paint Stocks and Crude Oil Tango?

BSE Broad and Sectoral Indices Returns

Real Estate Stocks and REITs

When Will Federal Reserve Raise Interest Rates?

The Central Triad in Taleb's Antifragile

Weblinks and Investing

-------------------

Those interested for a detailed analysis of bank disintermediation and flow of private sector resources may refer to my article written in 2020.

In this article, I'm providing just an update with data available up to financial year 2020-21.

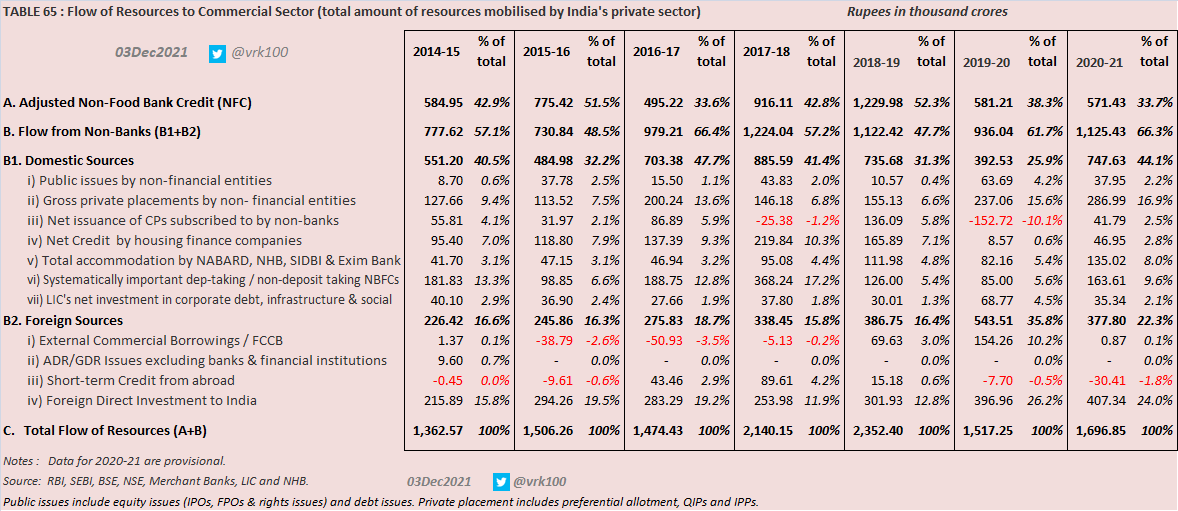

Chart providing data from 2014-15 to 2020-21 (click on the image for larger picture) >

During 2020-21, the money flow to the commercial sector increased by 11.8 per cent to Rs 16.97 lakh crore (Rs 15.17 lakh crore in 2019-20), showing an absolute growth of Rs 1.80 lakh crore -- of which major growth is from commercial paper issued by non-banks (row B1 iii), credit from NBFCs and accommodation by all-India financial institutions, such as, NABARD, NHB, etc.

Interestingly, money raised from ECBs is almost nil in 2020-21, while growth in FDI is just Rs 10,000 crore. The share of foreign sources fell to 22 per cent of the total flow in 2020-21 from 36 per cent in 2019-20.

As can be gleaned from the above table, the private sector's reliance on bank credit has come down from 42.9 per cent in 2014-15 to 33.7 per cent in 2020-21, as per data from Reserve Bank of India (RBI). The share of bank credit in total resources fluctuated between 34 per cent and 52 per cent of total flow in the past six years.

The media often highlight the fact that bank credit growth is tepid, as if it is the only source of funding for the commercial sector. As we've seen, the importance of bank credit for the growth of commercial sector in India has come down drastically over the years and as such you may correct the ignorant media above this.

- - -

References:

RBI Handbook of Statistics on Indian Economy 15Sep2021

Table 65: Flow of Resources to the Commercial Sector in India

My tweet dt 26Sep2020 on Flow of Resources to the Commercial Sector

My tweet dt 15Sep2018 on Flow of Resources to the Commercial Sector

RBI Mint Street memo dated 03Jan2018 Credit Disintermediation from Banks - Has the Corporate Bond Market Come of Age?