Bank Disintermediation and Flow of Resources to Private Sector-VRK100-26Sep2020

(Update dated 03Dec2021 of this article is available)

Private sector in India raises resources from a

variety of sources. Private sector includes both the corporate sector and

households. The corporate sector raises monies traditionally from banks. Over

the years, they have diversified their sources. Now, they tend to raise

resources from domestic sources, such as, non-banking finance companies (NBFCs)

and stock market. Routes for raising money from stock market include: initial

public offers - IPOs; follow-on public offers - FPOs; rights issues or through

private placement (like, qualified institutional placement or QIP).

A related topic in corporate finance is

pecking order theory, which shows the order in which corporates prefer to raise

resources. As per pecking order theory, it is cheaper and easier for corporates

to obtain resources internally. So, the first order of preference is raising

internal resources. And the second in line is debt, because cost of debt is

cheaper, due mainly to tax efficiency, versus cost of equity. And the last in

line is equity after exhausting the first two options.

The private sector raises resources from external

sources also, via foreign currency loans in the form of foreign currency

convertible bonds (FCCBs) and external commercial borrowings (ECBs). More importantly, Indian corporates attract a lot of money from foreign direct investment (FDI) route.

Financial

market professionals (FMPs) often focus on bank credit growth rate, which is a

high frequency indicator. With rapid changes in bank disintermediation, credit

to the private sector is now dominated by non-bank sources. As a result, bank

credit growth numbers have become less relevant in India like their Western

counterparts. When we say bank credit growth rate has fallen to 5% or 6%, it

conveys little meaning.

Bank disintermediation means raising of

resources by the private sector (both the corporate as well as households) from

entities other than banks. This disintermediation, started in the early 1990s,

has been going on with the share of non-banking sources growing rapidly in

recent years.

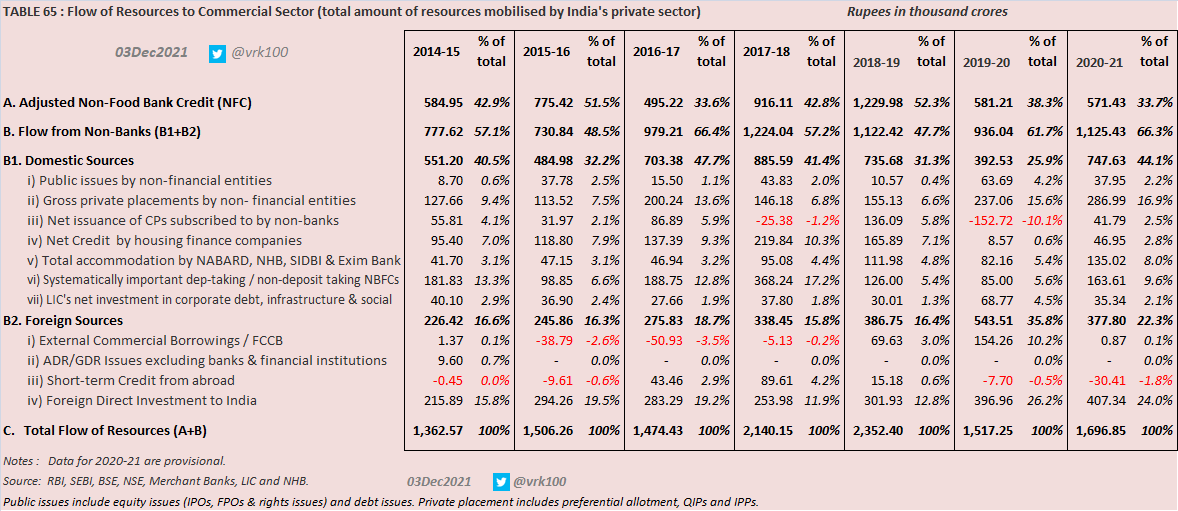

Chart providing data from 2009-10 to 2019-20 (click on the image for larger picture) >

As can be seen from the above table, the

private sector's reliance on bank credit has come down from 42.9% in 2014-15 to

40.2% in 2019-20, as per data from Reserve Bank of India (RBI). The share of

bank credit fluctuated between 34% and 52% of total flow in the past five

years.

Large sums of money have flowed into debt

mutual funds in recent years. As a result, mutual funds' role in providing resources

through bond investments in the corporate sector has gone up considerably as

can be observed from steep rise in assets managed by the mutual funds, which

typically invest in bonds of companies, NBFCs and HFCs.

Changes in FY 2019-20 compared to FY 2018-19:

As can be seen from the above table, resources

mobilisation by the private sector declined drastically in 2019-20.

Total

flow of resources to commercial sector fell by 39% in 2019-20 to Rs 14.46 lakh crore from Rs 23.52 lakh crore in 2018-19--this decline has adversely impacted

India's GDP growth. The fall is mainly due to steep fall in bank credit by 53% to Rs 5.81 lakh crore and fall

in commercial paper (CP) issuance. Others that contributed to the decline are

credit by HFCs (95% fall to just Rs 8,600 crore loan disbursement) and NBFCs (89% fall to just Rs 13,600 crore).

Post

IL&FS scam, loan disbursals by housing finance (HFCs) and non-financial

banking companies (NBFCs) got decimated. Commercial banks too are having their own problems especially public sector banks (PSBs). Stung by high percentage of bad loans, PSBs are extremely averse to

lending. Another issue that deters PSBs from lending is the onerous scrutiny of

bad loans by central government enforcement agencies, such as, Central Vigilance Commission

and others.

One bright

spot for corporates in 2019-20 is foreign direct investments (FDI) into India, which

surged by 32% to Rs 3.97 lakh crore. LIC of India's debt investments increased by nearly 130% to Rs 69,000 crore, which is the highest in the last 10 years.

Public

issues and private placements too have shown significant rise. External flows

from ECBs and FCCBs went up by more than 120% to Rs 1.54 lakh crore in 2019-20.

Lower

finance from banks and NBFCs has negatively impacted the automobile sector--which

depends heavily on finance.

In

the past five years, flows from domestic sources have fallen by more than 40% to Rs 3.21 lakh crore in 2019-20,

while flows from external sources have increased by 140% to Rs 5.44 lakh crore, signifying India's

dependence on foreign money.

- - -

P.S.: Updated data which include data for 2020-21 >

References:

My tweet dt 26Sep2020 on Flow of Resources to the Commercial Sector

My tweet dt 15Sep2018 on Flow of Resources to the Commercial Sector

RBI Mint Street memo dated 03Jan2018 Credit Disintermediation from Banks - Has the Corporate Bond Market Come of Age?

RBI Handbook of Statistics on Indian Economy 18Sep2020

Table 68: Flow of Resources to the Commercial Sector in India

Disclosure: I've vested interested in Indian stocks. It's safe

to assume I've interest in the stocks discussed, if any.

Disclaimer: The analysis and opinion provided here are only for

information purposes and should not be construed as investment advice.

Investors should consult their own financial advisers before making any

investments. The author is a CFA Charterholder with a vested interest in

financial markets. He blogs at:

http://scribd.com/vrk100

Twitter @vrk100