--------------------------------------------------------------

Update 09Jun2026: Chart 197:

Rupee Depreciation and India FPI Equity Flows: Correlation, Narrative and Reality:

The current narrative is that foreign portfolio investors (FPIs) are pulling money from Indian equity market because global capital is chasing the AI boom (especially in Taiwan, South Korea and the US tech), while India's earnings growth has disappointed and valuations remain relatively rich.

Rupee weakness versus dollar and other major currencies is cited as an additional headwind because it reduces dollar returns for foreigners.

Let us check whether the claim of experts regarding rupee depreciation is suported by long term data. This study covers the period from 2013 to 2026 (data till May2026).

CORRELATION YEARS:

The strongest apparent correlation is in 2018, 2022, 2025 and 2026: large FPI outflows from Indian stock market occurred alongside significant rupee depreciation. These years fit the narrative that foreign selling and rupee weakness moved together.

NO-CORRELATION YEARS:

2013 is the biggest contradiction: the rupee depreciated sharply (-11.5%) versus the dollar, yet FPIs bought a large USD 20 billion of equities.

Similar contradictions appear in 2014, 2015, 2016, 2019 and 2020, where the rupee weakened but FPIs were net buyers, bringing in dollars to India.

These years suggest rupee depreciation alone does not determine FPI behavior.

GLOBAL RISK-OFF YEARS:

From the chart alone, 2018 and 2022 stand out as the clearest risk-off years because they combine substantial FPI outflows with sharp rupee depreciation. Those were global liquidity events, not merely India currency events.

2018: Fed tightening, stronger dollar, emerging-market stress.

2022: Aggressive US rate hikes, strong dollar, global risk aversion.

2025 and 2026 were particularly painful for India, because other markets were doing well, while India is the worst performaing among the emerging markets.

In contrast, 2013 looks like a stress year for the currency but not a risk-off year for foreign investors, since FPI inflows remained very strong.

OVERALL MESSAGE:

The chart shows that rupee depreciation and FPI outflows sometimes occur together (2018, 2022, 2025, 2026), but there are also several years when FPIs invested heavily despite significant rupee weakness (especially 2013, and also 2014–16, 2019 and 2020).

This suggests that rupee depreciation by itself has not been a reliable long-term predictor of FPI flows.

However, financial markets are driven not only by fundamentals but also by narratives and momentum.

In the short to medium term, a narrative such as "the rupee is weakening, so dollar returns from India are deteriorating" can become self-reinforcing and influence capital flows even if the long-run historical relationship is weak.

The current episode is also different from many past years because investors are looking at a cumulative rupee depreciation of roughly 10 per cent over the last 18 months rather than a typical 2–4 per cent annual move.

When combined with concerns about earnings growth, valuations and the attractiveness of AI-related opportunities elsewhere (like Taiwan, South Korea and the US Tech), the currency move becomes much more meaningful for dollar-based investors.

Therefore, the data do not support the claim that rupee depreciation is a standalone driver of FPI outflows.

But it is entirely plausible that, in the current environment, a sizeable currency decline is amplifying a broader negative narrative and contributing to short- and medium-term foreign selling pressure.

Chart 197 showing FPI flows into Indian equity market verus Dollar Rupee Exchange rate Change (calenda year wise data from 2013 to 2026) >

--------------------------------------------------------------

Update 09Jun2026: Chart 196:

FPI Equity Flows to India: India

FPI Flows to Indian stock market, DII Flows to Indian stock market and

Individual Investor flows to India stock market - both in rupee terms as

well as dollar terms (old blog 10Jul2022) >

One chart:

1) calendar-year wise data from 2013 to 2026 >

Overview:

This

analysis looks at who has been putting money into Indian equity

markets—foreign investors (FPIs), domestic institutions (DIIs) and

individual investors—across different time periods.

The FPI selling of Indian equities continues unabated. The data in the chart are upto Apr2026.

In May2026, they sold stock worth Rs 33,000 crore and in this month (with only one week completed) alone they already sold equities worht Rs 56,000 crore.

--------------------------------------------------------------

Update 26Apr2026: Charts 194 and 195:

FPI Equity Flows to India: India

FPI Flows to Indian stock market, DII Flows to Indian stock market and

Individual Investor flows to India stock market - both in rupee terms as

well as dollar terms (old blog 10Jul2022) >

Two charts:

1) financial year wise data from 2014-15 to 2025-26

2) calendar-year wise data from 2013 to 2026 >

Overview:

This analysis looks at who has been putting money into Indian equity markets—foreign investors (FPIs), domestic institutions (DIIs) and individual investors—across different time periods.

By comparing yearly data with 3-year, 5-year and 10-year totals, it shows how market leadership keeps changing rather than staying constant.

Across FY2014-15 to FY2025-26, DIIs have invested over Rs 24 lakh crore (USD 295 billion), far exceeding FPIs at Rs 1.78 lakh crore (USD 34.0 billion), with individuals at Rs 3.55 lakh crore (USD 43.0 billion).

The shorter-term aggregates make this shift even clearer, highlighting the recent dominance of domestic money in driving markets.

Counterweight Phase: FY2020-21 and FY2021-22:

FY2020-21: FPIs bought Rs 2.74 lakh crore or USD 37.0 billion, while DIIs sold Rs 1.32 lakh crore or USD 18.0 billion.

FY2021-22: FPIs sold Rs 1.40 lakh crore or USD 18.5 billion, while DIIs bought Rs 2.22 lakh crore or USD 29.6 billion.

This is the textbook counterweight phase—flows offset each other, maintaining balance. This behavior historically defined Indian markets when foreign flows influenced marginal pricing.

Note: Every sell in the market is matched by a buy, so “counterweight” does not refer to existence of buyers. It refers to who provides incremental net demand that influences price direction and absorbs sustained selling pressure.

Shift to Domestic Dominance: Last 3–5 Years:

Past 3 years: FPIs at Rs -1.00 lakh crore, DIIs at Rs 16.65 lakh crore, Individuals at Rs 1.67 lakh crore.

Past 5 years: FPIs at Rs -2.77 lakh crore, DIIs at Rs 21.41 lakh crore, Individuals at Rs 3.81 lakh crore.

This marks a structural shift. Instead of counterbalancing, DIIs are overwhelming FPI selling. The magnitude is disproportionate—domestic flows are multiples of foreign outflows, indicating markets are being driven internally.

Recent Two-Year Pattern: FY2024-25 and FY2025-26:

FY2024-25: FPIs sold Rs 1.27 lakh crore or USD 14.6 billion; DIIs bought Rs 6.08 lakh crore or USD 71.8 billion.

FY2025-26: FPIs sold Rs 1.81 lakh crore or USD 19.7 billion; DIIs bought Rs 8.50 lakh crore and USD 95.8 billion.

These two years exaggerate the current regime. DII inflows are not just offsetting—they are significantly larger, pointing to strong domestic liquidity driving markets beyond foreign influence.

Over the past 12 years, total DII inflows are about USD 295 billion. Of this, nearly USD 168 billion—more than 50 percent—has come in just the last two financial years.

This indicates a sharp acceleration in domestic institutional participation, with flows becoming heavily concentrated in the most recent period rather than being evenly distributed over time.

Synchronized Buying Phase: FY2023-24:

FPIs bought Rs 2.08 lakh crore and USD 25.3 billion; DIIs bought Rs 2.07 lakh crore and USD 24.9 billion.

This is a rare alignment phase where both global and domestic liquidity were supportive. Such phases are typically short-lived and linked to strong momentum.

Long-Term Context: 10-Year View:

Past 10 years: All the three categories of investors had positive flows, with FPIs at Rs 0.81 lakh crore, DIIs at Rs 23.54 lakh crore, Individuals at Rs 3.67 lakh crore.

Over a full cycle, FPIs appear nearly neutral. DIIs dominate structurally, while individuals contribute but do not lead. This challenges the perception of sustained FPI dominance.

Individual Investors' Trend:

Up to FY2019-20: negligible or negative participation.

FY2020-21 to FY2022-23: surge Rs 0.68 lakh crore, Rs 1.65 lakh crore, Rs 0.49 lakh crore.

FY2023-24 to FY2025-26: cooling Rs 0.47 lakh crore, Rs 1.25 lakh crore, Rs -0.06 lakh crore.

Aggregate view: Rs 3.81 lakh crore over 5 years vs Rs 1.67 lakh crore over 3 years. Retail participation spiked post-2020 and is already fading, reinforcing that it is sentiment-driven, not permanent.

What Changed in the Latest Cycle:

The defining shift is the scale and persistence of domestic flows. Earlier, DIIs acted as a counterweight; now they dominate. This is evident in both yearly spikes and aggregated 3-year and 5-year data.

Will Current Trends Sustain?

Unlikely in a straight line. Counterweight phases will return when domestic flows weaken, synchronized buying will reappear during global liquidity expansions and retail participation will revive and fade with new narratives.

The 10-year data already shows how dominant trends normalise over time.

Bottom Line:

There are no permanent trends in markets. Leadership rotates across FPIs, DIIs and individuals depending on liquidity, returns and sentiment. The current dominance of domestic flows is real—but it is still a phase, not a permanent structure.

Tweet 26Apr2026 - error in NSE data, rectified by them after being pointed out

FPIs are foreign portfolio investors.

DIIs are domestic institutional investors.

According

to NSE India, DIIs include Banks, Insurance companies, Mutual Funds,

Domestic Financial Institution (Other than banks & insurance),

Domestic Venture Capital Funds, AIFs, PMS clients, New Pension System

(NPS) and NBFCs.

Individual

investors data for NSE secondary market only. Individuals include

individual /proprietorship firms, HUF (Hindu Undivided Family) and NRIs

(Non resident Indians).

Charts 194 and 195 click on the images to view better >

--------------------------------------------------------------

Update 24Apr2026: Charts 192 and 193:

FPI AUC data: FPI / FII AUC data: Assets under custody (AUC) data of foreign portfolio investors (FPIs):

Two charts >

FPI equity assets - Yearly data (past 10 years, financial year wise)

FPI debt assets - Yearly data (past 10 years, financial year wise) (for old data > Old blog dated 10Jul2022 - Exit India Policy by Foreign Investors; and old blog dated 28Apr2022 - Foreigners' Shrinking Pie in Indian Equities)

FPI

equity assets, as on 31Mar2026, are Rs 62.5 lakh crore, down from Rs 66.8 lakh crore as of 31Mar2025 -- due to a combination of stock market losses, sharp fall in Indian rupee versus dollar and massive FPI outflows in FY 2025-26 (Check Update 24Apr2026 with Charts 186 to 191 below for FPI equity flows and debt flows too).

FPI assets in India's equity segment are USD 660 billion in Mar2026, down a massive 30 per cent in the past 18 months (USD 930 billion in Sep2024).

FPI investors have been losing interest considerably in Indian stocks in the past five years -- their share has come down

from almost 20 per cent in Mar2021 to just 15.1 per cent now; conversely, domestic

investors' share has been rising gradually during the period.

FPI debt asets as of 31Mar2026 are Rs 7.1 lakh crore or USD 74.6 billion.

For a country of the size of India, FPI assets in the debt segment are a piffling USD 75 billion.

India stands out among emerging markets for its relatively low level of foreign participation in the domestic bond market, especially when compared with economies like South Korea, China and Brazil.

According to some estimates, foreign ownership of government bonds is less than 3 per cent of India's total public debt.

In comparison, the share of foreign participation in countries like, South Korea, China and Brazil is between 10 per cent and 20 per cent.

Data source:

Charts 192 and 193 >

--------------------------------------------------------------

Update 24Apr2026: Charts 187 to 191:

FPI Equity Flows to India: India

FPI Flows to Indian stock market and debt market in rupee terms > (old blog 10Jul2022) >

During the financial year 2025–26, FPI equity flows were negative in seven months, including a record monthly outflow of Rs 1.18 lakh crore in Mar2026—the highest in the 34-year history of FPI investments in India.

Although flows were positive in five months, the overall balance for FY 2025–26 turned into a net outflow of Rs 1.81 lakh crore, driven largely by the sharp outflows in Mar2026. Even in Apr2026 too, FPIs already sold stocks worth Rs 0.41 lakh crore, with another week to go this month.

In

the debt segment, the flows were better, with FPIs being net positive

in nine months, with the FY 2025-26 total inflows amounting to Rs 0.28 lakh crore.

Cumulative FPI flows to Indian equity markets are negative in the past five financial years.

As on 31Mar2026: Rs lakh crore

Past one year FPI equity flows -1.81

Past two year -3.08

Past three year -1.00

Past five year -2.77

Past 10 year 0.84

FPI debt flows are a saving grace for India, especially in the past three years.

As on 31Mar2026: Rs lakh crore

Past one year FPI debt flows 0.28

Past two year 1.75

Past three year 3.06

Past five year 3.21

Past 10 year 3.53

Some possible reasons why FPIs have been selling Indian equities:

Foreign investors have a whole variety of countries to invest in. India, now, is not the only play for them.

As investors have become enthusiastic about AI boom and massive bets on AI infrastructure, foreign investors find emerging markets like, South Korea and Taiwan more promising and these two countries have been receiving inflows, while foriegners have been selling Indian stocks.

In the six quarters alone (period Oct2024-Mar2026), FPIs sold Indian equities worth nearly Rs 4 lakh crore -- this is one of the highest outflows the country has witnessed.

Even some investors find Brazil market too more attractive due to its commodity play. China too has attracted more inflows.

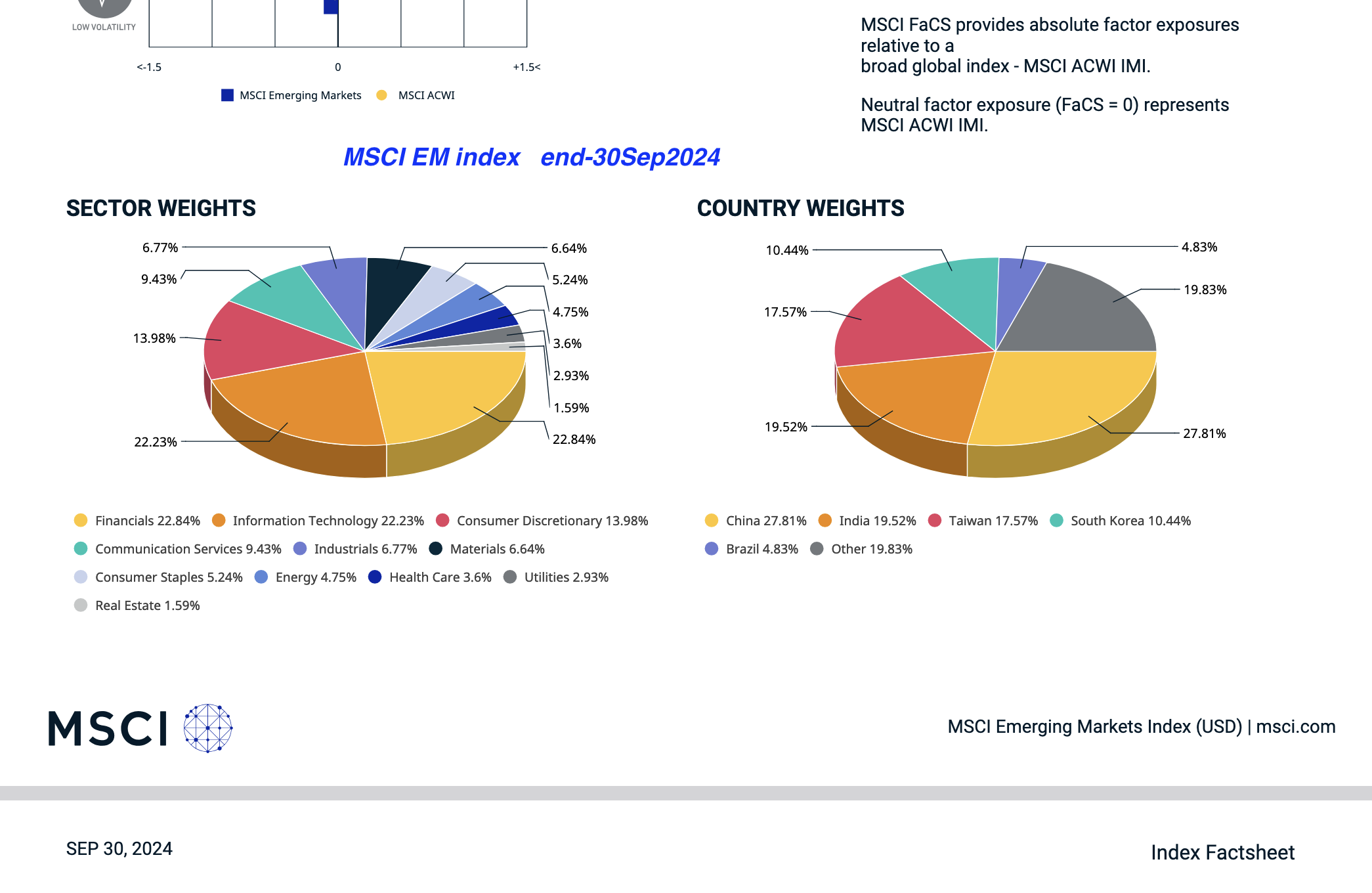

India is so negative in the eyes of FPIs, its share in the MSCI EM index declined from nearly 20 per cent (second rank in the index then) to 12.6 per cent in Mar2026 (4th rank now) (check update 22Apr2026 with Chart 186 below).

Corporate earnings growth has decelerated recently. As such, foreigners have turned lacklustre towards Indai. FDI flows too have not been encouraging in the past four years.

Indian governments are focusing more on doles, rather than building for the future.Rupee depreciation and earnings concerns too have weighed on FPIs.

Key factors influencing FPI flows (not just taxes) >

Relative valuation of Indian stocks

Political stability

Reliability of legal / judicial systems

Currency stability / forex risk

Interest rate differentials

Liquidity & market depth (ease of entry & exit)

Corporate governance

FPIs are foreign portfolio investors.

Five charts >

India FPI flows (both equity and debt) financial year wise

India FPI equity flows monthly (15 months)

India FPI equity flows quarterly (15 quarters)

ndia FPI debt flows monthly (15 months)

India FPI debt flows quarterly (15 quarters)

Charts 187 to 191 click on the image to view >

--------------------------------------------------------------

Update 22Apr2026: Chart 186:

MSCI EM Index - China and India weights: Quarterly changes between Dec2024 and Dec2025: (for old data, see old blogs dated 07Jan2023 and blog 03Aug2021 and previous charts below)

Overview:

MSCI Emerging Markets Index composition remains stable in breadth (24 countries) as of 31Mar2026. Market cap is broadly flat QoQ (quarter on quarter) but shows YoY (year on year) growth of nearly 30%, indicating recovery and capital inflows over the past year.

Market Capitalisation increase YoY reflects improved valuations and market performance across EM.

Valuation Metrics:

Forward P/E: Significant compression QoQ (11.52 vs 13.48) and modest decline YoY (11.52 vs 11.96), suggesting cheaper valuations recently after a period of optimism.

Price-to-Book: Stable QoQ (2.2), but up YoY (2.2 vs 1.8), indicating higher asset valuation multiples over the year.

Dividend Yield: Slight improvement QoQ (2.32% vs 2.28%), but lower YoY (2.32% vs 2.65%), implying some shift toward growth over income.

Country Weights:

QoQ: China weight declined sharply (25.48% vs 27.63%), while Taiwan and South Korea gained; India weight decreased notably (12.58% vs 15.30%).

YoY: China weight significantly lower (25.48% vs 31.29%), India also reduced (12.58% vs 18.52%), while Taiwan and South Korea gained share—indicating rotation away from China/India dominance toward North Asia tech-heavy markets.

Concentration Trends (Countries):

Top 5 concentration remains high, but internal reshuffling shows declining China dominance and rising importance of Taiwan semiconductor exposure and South Korea.

Top Companies:

QoQ: TSMC weight increased materially (13.29% vs 11.88%), reinforcing concentration risk; Tencent and Alibaba weights declined; Samsung relatively stable.

YoY: TSMC dominance sharply higher (13.29% vs 8.6%), while Chinese tech (Tencent, Alibaba) weights declined overall, indicating a shift toward semiconductor leadership.

Concentration Trends (Stocks):

The index is becoming more top-heavy, meaning a few large companies—especially TSMC—now have a bigger influence on performance. The weight of this single stock is more than the country weight of India, Brazil and others. Only country weights of China, Taiwan and South Korea are greater than the TSMC weight.

To sum up:

QoQ: Valuations corrected downward, China and India weights reduced, and semiconductor exposure increased.

YoY: Strong market cap growth, declining China dominance, rising Taiwan/Korea influence, and increasing concentration in a few mega-cap tech names led by TSMC.

Chart showing MSCI EM Index matrix showing data fo rthe past five quarters >

--------------------------------------------------------------

Update 01Apr2026: Charts 184 and 185:

Global market data: Global market data pertaining to stocks, bonds,

commodities and currencies are presented here (old blog dated 29Jun2024).

Quarter-to-date

(QTD) global market data, as on 31st of March, 2026, of stocks, bonds,

currencies and commodities is as follows:

During Jan-mar2026 quarter (QTD),

the stand-out performance from crude oil, WTI and Brent have skyrocketed by 78 and 94 respectively (note Bloomberg / Trading Economics are showing divergent rates for Brent, as of 31Mar2026, for unknown reasons -- CNBC rate is considered for the analysis).

Gold and silver experienced subdued returns, after spectacularly well in 2025. Bitcoin continues to disappoint this quarter too.

Stock marekts globally are mostly down, driven by Iran war concerns. Only, FTSE and Nikkei posted meagre gains.

Indian stock are one of the worst performing in the quarter.

Bond yields are rising globally, due to geopolitical risks to world economy emanating from a raging war in the Middle East. Inflationary expectations have surged due to higher oil prices.

US dollar index (DXY) rose by 1.7 per cent, with dollar gaining vs JPY, EUR and GBP.

Indian currency is one of the worst performing among emerging markets. India, a commodity importer, is adversely impacted by the Third Gulf War.

Past one year returns: In the past one year, silver and gold delivered spectacular returns of 122 and 49 per cent respectively. So is crude oil.

Bloomberg commodity index delivered a return of 27 per cent.

In stocks, Nikkei 225, Nasdaq Composite, Shanghai and FTSE 100 provided superior returns.

Indian stocks are a disappointment.

The US dollar index lost 4 per cent of its value in the past one year. While the dollar gained versus JPY, it depreciated against Euro and British Poound.

The one year return (YTD) chart is also attached below.

QTD and one-year returns >

--------------------------------------------------------------

Update 31Mar2026: Chart 183:

Dollar Rupee exchange rate: USD INR Exchange Rate: Financial year-wise data of the US dollar-Indian rupee exchange rate for the past 28 years (previous blog dated 03Jun2024 on Why RBI Won't Favour a Strong Rupee and preivous blog dated 01Jun2024 on how to calculate currency depreciation and appreciation) >

USD-INR yearly gain / loss

Exchange rate yearly gain / loss

Dollar rupee yearly gain / loss

USD-INR financial-year and calendar-year end data

USD-INR change %:

Financial year-wise: Dollar gain versus Rupee: Data include not only year-wise changes but

also 5-year change (annualised) and 10-year change (annulised or CAGR).

For example, between end-Mar2021 and

end-Mar2026, the USD appreciated by 5.2 per cent annualised rate. And

between end-Mar2011 and end-Mar2016, the annualised USD appreciation vs

INR was much higher at 8.2 per cent.

Likewise, between end-Mar2016 and end-Mar2026 (10 year range), the USD appreciated by 3.6 per cent annualised rate (CAGR).

For the past 25 years, US dollar has appreciated by an annualised 2.87 per cent versus India rupee.

Data range for FY-wise yearly change

for the past 27 years is: minus 11.4 per cent to plus 27.5 per cent.

The data range is so wide one can't even predict / forecast the yearly

changes in USD-INR exchange rate.

Of

the 27 financial years for which data are presented here, Govt of India

and Reserve Bank of India allowed the rupee to appreciate against the

dollar only on eight occasions.

Data for USD–INR are from RBI DBIE. All other calculations are by the author.

Explanation for two columns in the two tables presented below >

Column 3 (USD–INR change %):

This shows how much the value of one US dollar changed compared to the

Indian rupee during the year. A positive number means the dollar became

stronger (it took more rupees to buy one dollar). A negative number

shows the dollar depreciation versus rupee (dollar became weaker).

Column 7 / extreme right (INR–USD change %):

This shows how much the value of one Indian rupee changed compared to

the US dollar during the year. A positive number shows the rupee

appreciation (one rupee could buy more dollars). A negative number means

the rupee became weaker versus the dollar.

To know more about the currencies and how to calculate depreciation and appreciation of currency pairs, please check previous blog.

Long term trends:

The USD-INR exchange rate shows a clear long-term uptrend, meaning the Indian rupee has steadily depreciated against the US dollar over the past 25+ years. The rate moved from around 42–44 in the early 2000s to about 94.7 by Mar-2026.

The rupee saw a sharp depreciation in FY2025-26, with USD rising 10.7 per cent to 94.7 (conversely rupee depreciated by 9.6 per cent). This is one of the steepest annual moves in the dataset, comparable to crisis-like periods, like, COVID-19, Fed taper tantrum or global financial crisis (GFC) of 2008.

Periods of Sharp Depreciation:

From the 27 financial years shown (FY2000–FY2026), the US dollar gained (conversely, rupee depreciated) more than 8 per cent against the Indian rupee on six occasions.

Major stress years stand out clearly: FY2008-09 (27.5% dollar appreciation vs 21.6% rupee depreciation), FY2011-12 (12.7% rupee depreciation), FY2013-14 (9.5% rupee depreciation), FY2019-20 (8.2% rupee loss), FY2022-23 (7.8% rupee loss), and FY2025-26 (9.6% rupee depreciation).

Six out of 27 years is roughly 22 per cent of the time (about one in every 4–5 years). This shows that sharp depreciation events are not rare—they occur periodically as part of broader economic cycles. These events are not evenly spaced; they tend to cluster around stress periods.

Key Takeaway:

While average annual depreciation may look moderate, the distribution is skewed—large moves happen in bursts. Any long-term view of USD-INR exchange rate must account for these occasional but impactful spikes.

Implications of rupee depreciation for NRIs (non resident Indians), especially those who live in America:

Core Idea in Simple USD-INR Terms:

Think of it this way: what cost Rs 47 per USD earlier in 2011/12 now costs about Rs 95 per USD. The rupee has roughly halved in value in the past 14–15 years. So if an NRI converted USD into Indian rupees back then, their money—when viewed in US dollar today—has effectively been cut in half unless the asset they bought has grown enough to compensate.

Illustration: The Rs 47 to Rs 95 Reality

Around FY2012, 1 USD ≈ Rs 47.

Today, it appreciated to Rs 95.

Example:

USD 100,000 in 2012 → Rs 47 lakh invested in India

Today, Rs 47 lakh converts back to only about USD 50,000

So purely due to currency movement, the dollar value is roughly halved.

This is the “hidden loss” NRIs often miss because they track wealth in rupees.

What Must Happen to Break Even:

To just get back the original USD 100,000, that Rs 47 lakh must become about Rs 95 lakh today.

In simple terms:

Your investment must double just to break even in USD.

Anything less than doubling = loss in USD

Anything more than doubling = real gain in USD

So the real question is not “did my asset go up?” but “did it go up enough to offset the rupee fall?”

5-Year Example (Recent Reality):

5 years ago, USD INR was around Rs 75–76; today nearly Rs 95.

Example:

USD 100,000 → Rs 75 lakh → now worth only USD 79,000 if no growth in the underlying asset.

Even in just 5 years, you lose around 20 percent in USD terms without asset growth.

So your asset must grow from Rs 75 lakh to about Rs 95 lakh just to stand still.

10-Year Example:

10 years ago, USD-INR was around Rs 62–65; today Rs 95.

Example:

USD 100,000 → ~Rs 63 lakh → now USD 66,000 if unchanged.

You need Rs 63 lakh to become Rs 95 lakh (about 50 percent growth) just to break even.

15-Year Perspective:

15 years ago, USD INR was around Rs 45–47; today Rs 95.

Example:

USD 100,000 → Rs 46 lakh → now roughly USD 48,000–50,000.

You need the asset to roughly double over this period just to maintain USD value.

20-Year Perspective:

20 years ago, USD-INR was around Rs 43–45; today Rs 95.

Example:

USD 100,000 → Rs 44 lakh → now about USD 46,000.

Again, nearly two times growth required just to preserve dollar value.

25-Year Perspective:

25 years ago, USD-INR was around Rs 42–43; today Rs 95.

Example:

USD 100,000 → Rs 43 lakh → now about USD 45,000.

Same conclusion: the rupee has roughly halved, so assets must double just to break even in USD terms.

What This Means for Different Assets?

If your Indian asset:

Did not double over 10–15 years → you lost money in USD

Just doubled over 15 years → you barely broke even

Tripled or more → you made real USD gains

This is why:

Equities (which can grow three to five times over long periods) can beat currency loss.

Real estate (often 1.5x–2.5x over long periods) may only break even or underperform in USD.

Why Many NRIs Misjudge This:

NRIs often think:

“I bought at Rs 50 lakh, now it’s Rs 1 crore — I doubled my money.”

But in USD terms:

Rs 50 lakh (at Rs 50 per USD) ≈ USD 100,000

Rs 1 crore (at Rs 100 per USD) ≈ USD 100,000

So after many years, the “doubling” in rupees may just be currency illusion.

When It Still Makes Sense:

It works financially only if:

The asset grows well beyond two times over long periods (ideally 3x–4x or more)

It still makes sense regardless of returns if:

You plan to return to India

You want family/security/social roots

You want diversification outside USD assets

Key Point:

For NRIs, the move from around Rs 45 to Rs 95 per USD means:

Your benchmark is not “did my asset grow?”

It is “did my asset at least double?”

If not, your wealth in USD terms has quietly shrunk—even if in rupee terms it looks like a success.

Core Principle for NRIs: Separate Emotion from Financial Reality:

Investing is fundamentally about cold, objective calculations. Emotional comfort, family expectations, and a sense of belonging are real and valuable—but they are not financial returns. NRIs need to consciously separate these two worlds instead of mixing them.

Emotional Value Is Real—but Not Measurable.

Buying property or assets in India often gives peace of mind:

family feels secure, social standing improves and there is a psychological fallback option.

These are meaningful benefits. In many cases, they may even outweigh financial returns for the individual. But they cannot be measured in rupees or dollars, and they should not be mistaken for investment performance.

The Financial Reality NRIs Must Face:

From a purely financial lens, the math is unforgiving:

If Rs 47 per USD becomes Rs 95 per USD, your base currency has lost half its value.

So any asset bought in India must:

not just grow—but grow enough to overcome this currency gap.

If it doesn’t, then regardless of how good it “feels,” the investment has underperformed in USD terms.

Chart 183 click on the image to view better >

--------------------------------------------------------------

Update 20Mar2026: Chart 182:

FPI Equity Flows to India: India

FPI Flows to Indian stock market, DII Flows to Indian stock market and

Individual Investor flows to India stock market - both in rupee terms as

well as dollar terms - calendar-year wise data from 2013 to 2026 > (old blog 10Jul2022) >

Comparing CY 2025 with CY 2026 (both based on the first 2 months):

FPIs: Outflows are much smaller in 2026 (-1.5 billion USD) versus heavy selling in 2025 (-13.0 billion USD). This suggests foreign selling pressure has sharply eased in 2026.

However, in March 2026, with only six trading sessions remaining, FPI selling has accelerated sharply, with net outflows already reaching about USD 9.5 billion.

DIIs: Slightly lower in 2026 (11.9 billion USD) compared to 2025 (17.5 billion USD), but still strong and clearly positive. Domestic institutions continue to provide steady support, though at a slightly reduced pace.

Individuals: Noticeably weaker participation in 2026 (1.0 billion USD) versus 2025 (3.2 billion USD). Retail inflows have cooled meaningfully.

Overall: FPI selling in Indian stock market continues to be heavy in calendar year 2026 too. DIIs have been providing support to the market, though at a reduced pace compared to first two months of 2025.

Individual interest in 2026 has dwindled compared to the first two months of 2025.

In

the past five years, FPIs net outflow from Indian stocks is nearly USD 10.8 billion (Rs 90,000 crore); whereas DIIs net inflows in the same period are USD 222.9 billion (Rs 18.61 lakh

crore).

FPIs are foreign portfolio investors.

DIIs are domestic institutional investors.

According

to NSE India, DIIs include Banks, Insurance companies, Mutual Funds,

Domestic Financial Institution (Other than banks & insurance),

Domestic Venture Capital Funds, AIFs, PMS clients, New Pension System

(NPS) and NBFCs.

Individual

investors data for NSE secondary market only. Individuals include

individual /proprietorship firms, HUF (Hindu Undivided Family) and NRIs

(Non resident Indians).

Chart 182 click on the image to view better >

--------------------------------------------------------------

Update 18Mar2026: Charts 180 and 181:

FPI AUC data: FPI / FII AUC data: Assets under custody (AUC) data of foreign portfolio investors (FPIs): the two charts below are:

FPI equity assets - Quarterly data (past 12 quarters)

FPI debt assets - Quarterly data (past 12 quarters)

(for old data > Old blog dated 10Jul2022 - Exit India Policy by Foreign Investors; and old blog dated 28Apr2022 - Foreigners' Shrinking Pie in Indian Equities)

FPI

equity assets, as on 28Feb2026, are Rs 71.8 lakh crore, as compared to Rs 74.3 lakh crore on 31Dec2025.

FPI equity assets were USD 789 billion as on 28Feb2026, showing a decline of USD 36 billion compared to data as at end-Dec2025. This is due to fall of Indian indices and FPI selling between end-Dec2025 and end-Feb2026.

A

combination of heavy FPI outflows and Nifty 50 decline resulted in

share of FPI equity assets (FPI equity AUC) falling from 16.4 per cent (as a percentage of total market cap of

all BSE listed firms) in Sep2024 to 15.5 per cent in Feb2026.

FPI investors have been losing interest considerably in Indian stocks in the past four years -- their share has come down

from almost 20 per cent in Mar2021 to below 16 per cent now; domestic

investors' share has been rising gradually during the period.

In the charts below for equity AUC, you could find data relating to equity AUC in rupees and dollars, year-on-year percentage change in equity AUC in dollar terms, Nifty 50 level, year-on-year percentage changes in Nifty 50 and the US dollar - Indian rupee exchange rate.

FPI debt assets, as on 28Feb2026, are Rs 7.2 lakh crore, as compared to Rs 7.1 lakh crore on 31Dec2025.

FPI

debt assets were USD 79.3 billion as on 28Feb2026, showing stagnation in the past four to five months. As can be seen in the chart

attached below, the growth rates of debt assets have fallen during

2025, though total assets are growing.

Debt assets at USD 79.3 billion are nearly one-tenth of equity assets (USD 789 billion) as of 28Feb2026.

To a mild extent, the huge outflows of FPIs in equity segment have been compensated by inflows into debt segment.

In the charts for debt assets, you could find data relating to debt AUC in rupees and dollars, year-on-year percentage change in debt AUC in dollar terms, 10-year G-Sec yield and the US dollar - Indian rupee exchange rate.

Total

assets (including equity and debt) in India held by forign

portfolio investors (FPIs) as on 28Feb2026 are USD 868 billion as

compared to USD 1 trillion achieved as of 30Sep2024.

Charts 180 to 181 click on them to view better >

--------------------------------------------------------------

Update 15Mar2026: Charts 178 and 179:

Shipping trade data through Strait of Hormuz and Suez Canal (near Red Sea): Shipping traffic data through Strait of Hormuz and Suez Canal - Recent Trade Disruptions: International Trade Data:

Strait of Hormuz: Trade volumes through the Strait of Hormuz were within the normal historical range of about 2.6 to 3.7 million metric tonnes between 2023 and 2025.

By 28Feb026, the 7-day moving average trade volume had risen to about 4.07 million metric tonnes, indicating strong shipping activity.

But after the US - Israel joint war against Iran began on 28Feb2026, international trade through the Strait of Hormuz rapidly collapsed since 01Mar2026.

By 08Mar2026 trade volumes fell to only about 0.07 million metric tonnes, representing roughly a 98 percent drop within a week.

This data indicate that commercial shipping through the Strait of Hormuz has effectively come to a near halt due to the Third Gulf War.

The Strait of Hormuz is one of the most critical chokepoints in global trade because it is the main maritime gateway for exports from the Persian Gulf. Roughly one-fifth of the world’s crude oil and a large share of liquefied natural gas (LNG) shipments pass through this narrow waterway each day.

Any disruption to shipping in the strait can quickly affect global energy supply, transport routes and international trade flows.

Suez Canal (near Red Sea): The Suez Canal is another systemically important shipping lane that carries about 15 percent of global maritime trade and connects Europe and Asia through the Red Sea.

Before disruptions began, trade volumes through the canal were strong, with the 7-day moving average reaching about 3.42 million metric tonnes in mid-Dec2023.

However, attacks on commercial vessels in the Red Sea near the Bab el-Mandeb Strait starting on 16Dec2023 significantly disrupted shipping in the region. As a result, many shipping companies avoided the route and rerouted vessels around the Cape of Good Hope, leading to a sharp decline in trade flows through the Suez Canal.

By 20Nov2024, the 7-day moving average trade volume had dropped to about 1.02 million metric tonnes, representing a decline of 70 percent compared with the mid-Dec2023 level.

Trade volumes remained relatively low through 2025 but began to recover gradually as attacks from Houthi rebels in Yemen decreased.

By 03Mar2026, the trade volume had risen to about 1.59 million metric tonnes, though this was still around 53.4 percent lower than the level recorded before the disruptions began.

The Suez Canal and Bab el-Mandeb Strait faced major disruptions starting mid-Dec2023 due to attacks on commercial ships, in the Red Sea, by Houthi rebels.

The Houthis carried out attacks on commercial ships to retaliate against Israel and its allies and to assert leverage amid the Israel–Hamas war.

data sources:

Charts 178 and 179 click on the image to view better >

--------------------------------------------------------------

Update 04Mar2026: Charts 176 and 177:

FPI Equity Flows to India: India

FPI Flows to Indian stock market and debt market in rupee terms > (old blog 10Jul2022) >

Jan2026 experienced one of the heaviest FPI selling months for equity markets in India, with FPIs net selling amountng to nearly Rs 36,000 crore, though they turned positive in Feb2026 with inflows of Rs 22,600 crore.

FPI debt flows are a saving grace for India, especially in the past three years. During Jan2026 and Feb2026, debt flows by FPIs were positive after experiencing negative flows in Dec2025.

Significantly, in the past 12 months, nine months have seen positive debt FPI flows to India.

FPIs are foreign portfolio investors.

Two charts >

India FPI equity flows monthly (15 months)

India FPI debt flows monthly (15 months)

Charts 176 and 177 click on the image to view better >

--------------------------------------------------------------

Update 22Feb2026: Charts 174 and 175:

US Dollar Sale and Purchase by Reserve Bank of India: RBI USD Sale and purchase: RBI forex intervention / currency intervention: (old blog dated 05Aug2021 with monthly and yearly data for several years -- see also update 24Dec2025 with charts 150 and 151 below)

Two

charts showing monthly and quarterly data of USD sales and purchases by

RBI > Data avilable only till 31Dec2025 as RBI releases official

data on currency intervention with a two month gap >

Between Jun2025 and Dec2025, RBI has been net seller in all seven months,

with total net sale amounting to USD 53.4 billion, in order to defend a depreciating rupee (see charts below).

Despite the heavy RBI forex intervention, the rupee weakened by 4.94 per cent against the dollar during the same period, falling from 85.48 at end-May2025 to 89.92 by end-Dec2025.

Over these seven months (Jun-Dec2025), India’s foreign currency assets (FCA) declined by USD 24.6 billion - significantly lower than the RBI’s net dollar sales of USD 53.41 billion.

Possible reasons for lower reduction in FCA compared to RBI's net sales of US dollars:

The RBI’s net dollar sales of USD 53.41 billion reduced reserves mechanically, but FCA is marked-to-market, not a simple cash balance.

Valuation gains: from a weaker US dollar against other reserve currencies and/or rising global bond prices — likely lifted the USD value of non-dollar assets (denominated in Japanese Yen, Pound Sterling or Euro).

As a result, these positive valuation effects offset part of the intervention impact, keeping the FCA decline (USD 24.6 billion) well below net sales.

The RBI earns significant interest income from US Treasuries and foreign sovereign bonds, which constantly injects new capital back into the FCA.

The net sales figure includes future commitments (forward contracts), whereas the FCA only reflects actual cash movements and settled transactions.

Between end-May2025 to end-Dec2025, the US dollar

gained 5.2 per cent versus the Indian rupee -- conversely, INR lost

4.94 per cent vs the USD.

Since the start of 2025, rupee has been

volatile. It even appreciated to a level of 84 during the first week of

May2025.

Even

though, US dollar index (DXY), a guage of USD versus six major

currencies, had fallen only 1.2 per cent between end-May2025 and end-Dec2025, rupee has been under

pressure due to Trump tariffs, FDI slowdown and FPI heavy selling in Indian stock markets.

Charts 174 and 175 click to view better >

--------------------------------------------------------------

Update 27Jan2026: Chart 173:

RBI Gold Holdings as at the end of Nov2025: RBI

gold reserves are part of India's forex reserves maintained by RBI on

behalf of Government of India >

References:

Central Banks Fuel Gold Speculation, Risking Pain for Ordinary People 23Dec2025

Who is Eating my gold ETF return? 25Jan2022 (updates 20Jan2025 and other latest ones are available -- recency bias)

For more on RBI gold holdings, see blog dated 07Mar2022

Gold’s 2025 Rally Is Not a Central Bank Story:

As of 27Jan2026, gold has shattered records, recently crossing the historic USD 5,000 per troy ounce mark.

Central banks are not the marginal buyers setting gold prices, even though they matter for long-term credibility.

In calendar year 2025, global central bank gold buying slowed (compared to CY 2024). And, India's central bank, Reserve Bank of India (RBI), added only about 4 tonnes, which confirms they were not driving the rally (see chart below). Central banks buy slowly, often off-market.

Based on the purchases data, one could safely surmise that RBI took a strategic decision not to add anything further to its gold reserves, once international gold price crossed USD 2,800-3,000 per ounce level in Dec2024-Jan2025.

One caveat: While some central banks, notably China, may under-report or delay disclosure of gold purchases, available data suggest official buying was not the marginal driver of gold prices in 2025.

Gold prices move mainly on financial demand, not on slow-moving official central bank accumulation.

Since mid-2025, ETF (exchange traded fund) inflows, futures positioning and trend-following funds turned decisively bullish and pushed prices higher.

A few billion dollars of financial inflows can move gold prices far more than tens of tonnes of central bank purchases.

At the same time, markets may be pricing in weaker growth and falling real interest rates, which is historically the strongest driver of gold.

Private investors and institutions increased gold exposure as a hedge against currency risk, sanctions risk and portfolio volatility.

Geopolitical risks are adding a persistent risk premium to gold.

Ongoing but slower central bank buying provided a downside floor, encouraging speculative and leveraged long positions.

Poland central bank’s announcement that it plans to add 150 tonnes of gold, on top of its existing 550-tonne holdings, is a long-term strategic signal rather than evidence of near-term demand.

With no specified timeline, such purchases are typically spread over years and often executed discreetly, making them unlikely to drive sharp price moves.

These announcements mainly reinforce a downside floor for gold by validating official-sector support, but they do not explain the rapid price acceleration since mid-2025.

In short, the 2025–26 gold rally is being driven by financial investors and macro expectations, not by central banks.

Gold surge driven by currency debasement?

One of the strongest arguments propounded by gold investors is the currency debasement. In simple terms, debasement is the "hidden" erosion of a currency’s value caused by, ultra-loose monetary policies, excessive money printing and high government debt.

Government debt has gone up substantially over the years, especially, after the 2007/2008 Global Financial Crisis (GFC). Post-COVID fiscal stimulus in the US and Europe, funded by money creation, reinforced fears of long-term dilution of fiat currencies.

Rising and arguably unsustainable public debt levels in the US, Japan and Europe have further amplified the currency debasement concerns.

But what about bond markets and currencies?

Inflationary expectations currently are low. Bond yields also do not reflect any excessive stress from inflationary or geopolitical concerns (except in Japan, where bond yileds are rising recently driven more by political and fiscal uncertainty).

Inflation expectations remain relatively low, weakening the classic argument for gold as a pure inflation hedge. If inflation is not the driver, investors must ask what risk gold prices are actually signaling.

One interpretation is that markets are pricing in the possibility of major geopolitical conflict. Yet much of the global stress has not fully surfaced in sovereign bond markets or major currencies. The dollar index is down roughly 11 percent over the past year but is broadly unchanged over the past decade despite significant volatility.

This

points to short-term dollar weakness rather than an outright collapse

of the currency system. The gap between relatively stable long-term

currency trends and surging gold prices suggests fear of future regime

shifts rather than present-day data.

Sceptics of the debasement theory argue that gold’s recent surge is driven more by temporary speculative mania and geopolitical jitters than a permanent collapse of the monetary system.

Furthermore, history shows that central banks have successfully used interest rate hikes and quantitative tightening to tame inflation in the past, proving that fiat systems may be more resilient than gold enthusiasts suggest.

Ultimately, viewing gold as a diversified insurance policy rather than an inevitable replacement for currency helps temper the extreme narratives often found in the market.

Investors need to do some critical thinking:

What are the second-order and third-order effects of gold and silver prices reaching new all time highs (ATH) every day?

Will sovereign governments sit on their hands while their monetary sovereignty is threatened relentlessly?

Chart showing calendar year gold holdings of RBI, yearly growth and growth in per cent - world gold price is added to guess at what price RBI bought gold >

Chart 173 click to view better >

--------------------------------------------------------------

Update 22Jan2026: Charts 171 and 172:

India FDI flows: Foreign Direct Investment flows : Gross FDI flows and net FDI flows data (old blog 25May2022, Tweet thread 25May2022, Tweet thread 19Jan2024 and Tweet thread 16Jun2025 >

(see Update 08Sep2025 with good analysis)

(see Update 16Jun2025 with charts 91 and 92 below)

Net foreign direct investment (FDI) Flows to India: Net FDI rebounded sharply in the first 8 months of FY 2025-26 (see chart below for data):

A. Gross FDI to India:

Gross FDI to India rose to USD 64.7 billion in the first 8 months of financial year 2025–26, up 16.1 per cent over the same period last year.

This suggests renewed foreign investment interest at the entry level -- some of the growth is from huge foreign ownership interest in India's financial sector in 2025.

Mar2025: Singapore's Temasek takes 10% stake in India's Haldiram's for USD 1 billion. A few weeks later, Haldiram sold part stakes to IHC and Alpha Wave Global.

Global technology giants pledges:

US tech giants announced a lot of investmetns in India, such as:

> Amazon Inc / AWS committed investments of USD 35 billion by 2030 in cloud / AI infrastructure > Google / Alphabet to invest USD 15 billion in AI hub (data centre) in Visakhapatnam

These commitments suggest a strong pipeline of FDI inflows to India in the next five years.

B. FDI Repatriation / disinvestment declined but remains structurally high:

FDI repatriation fell 4.2 per cent year-on-year to USD 37.0 billion, indicating some easing of exit pressure. However, the absolute level remains large, confirming that private equity (PE) and venture capital (VC) exits and disinvestments are a dominant feature of India’s FDI cycle.

FDI repatriation mainly refers to the withdrawal of equity investments, including the return of invested capital, proceeds from selling shares and repatriation of reinvested earnings.

Foreign multinational companies (MNC) selldowns in Indian stock market in 2024 include: Hyundai Motors India (USD 3.3 bn IPO), BAT in ITC (USD 2.0bn), Whirlpool in its India arm (USD 0.5bn), Timken, Singtel-Bharti Airtel, Vodafone-Indus Towers and ZF Com Veh Control Systems India.

FDI repatriations in 2025: LG Electronics India (via USD 1.7 billion IPO) and PE firms exiting via IPOs of Lenskart Solutions, Meesho Ltd and Pine Labs.

IPO boom as an exit accelerator for foreign investors:

The roaring IPO market in India during 2024–25 and 2025–26 has likely acted as a powerful enabler of FDI repatriation, especially for PE and VC investors seeking public-market exits.

While not the sole driver, strong IPO valuations and deep domestic absorption have made it easier to monetise earlier FDI investments and repatriate capital.

C. FDI to India improved sharply from a low base:

FDI to India (gross minus repatriation) jumped 61.6 per cent to USD 27.7 billion. This improvement is driven more by lower repatriation than by a surge in fresh inflows, highlighting that FDI is highly sensitive to exit behaviour.

D. Outward FDI by Indian firms also accelerated:

FDI by India increased 34.9 per cent to USD 22.1 billion, reflecting stronger overseas investment by Indian corporates. This offsets a significant portion of inbound FDI.

Outward FDI by Indian firms include (some of them are yet to fructify):

> Tata Motors acquires Iveco (Italian truck maker) for USD 4.45 billion (final closing is subject to regulatory / funding approvals)

> Bharti Airtel's parent company, Bharti Global, invested USD 4 billion to acquire a 24.5% stake in BT Group

> Sun Pharma invested USD 829 million into its Netherlands subsidiary and has successfully acquired Checkpoint Therapeutics

> Dec2025: IT services giant TCS Ltd acquires 100% stake in US-based Coastal Cloud for USD 700 million

> Oct2025: Lupin Ltd announces plan to build a manufacturing plant in Coral Springs, Florida, USA at a cost of USD 250 million

> Aug2025: Zydus Wellness Ltd, a subsidiary of Zydus Lifesciences, on 29Aug2025 announced acquisition of UK-based Comfort Click Ltd (CCL) for a cash consideration of USD 320 million

E. Net FDI remains modest despite sharp percentage growth:

While the past three financial years (FY2023 to FY2025) have been a disaster (check the yearly data chart given below), net FDI flows to India stands at only USD 5.6 billion, though up more than seven times year-on-year due to a very low base last year.

Macro takeaway—FDI headline strength masks underlying churn:

The data show a high-churn FDI regime: strong gross inflows coexist with heavy repatriation and rising outward FDI.

For foreign exchange markets and the rupee, this means limited net dollar support despite healthy-looking gross FDI numbers.

Additional data:

PE exits from India in USD billion as per EY report:

22.2 in Jan-Jul2025

28.1 in 2024

24.9 in 2023

18.3 in 2022

39.6 in 2021

6.0 in 2020

Two charts showing gross FDI, FDI repatriation, FDI to India, outward FDI by India and net FDI flows: Data from 2006-07 to 2025-26 >

Data: RBI DBIE and author

Chart 171 click on the image to view better >

Chart 172 click on the image to view better: data from 2006-07 to 2025-26 >

--------------------------------------------------------------

Update 16Jan2026: Chart 170:

FPI Equity Flows to India: India

FPI Flows to Indian stock market, DII Flows to Indian stock market and

Individual Investor flows to India stock market - both in rupee terms as

well as dollar terms - calendar-year wise data from 2013 to 2025 > (old blog 10Jul2022) >

After

a gap of six years, individual investors turned negative (data up to

31Dec2025) in calendar year 2025. DIIs invested a record USD 89.6 billion (Rs 7.81 lakh

crore) in Indian equities in CY 2025.

Whereas,

FPIs exited Indian stocks worth USD 18.9 billion (Rs 1.66 lakh crore) in 2025, more than full calendar year outflows in 2022. Going by the past trend, FPIs

may turn positive in 2026 subject to a win-win trade deal between India

and the US, rupee stabilising and other factors.

In

the past five years, FPIs net outflow from Indian stocks is nearly USD 10.8 billion (Rs 90,000 crore); whereas DIIs net inflows in the same period are USD 222.9 billion (Rs 18.61 lakh

crore).

Calendar year 2025 data are upto 31Dec2025 (full year).

FPIs are foreign portfolio investors.

DIIs are domestic institutional investors.

According to NSE India, DIIs include Banks, Insurance companies, Mutual Funds, Domestic Financial Institution (Other than banks & insurance), Domestic Venture Capital Funds, AIFs, PMS clients, New Pension System (NPS) and NBFCs.

Individual

investors data for NSE secondary market only. Individuals include

individual /proprietorship firms, HUF (Hindu Undivided Family) and NRIs

(Non resident Indians).

Chart 170 click on the image to view better >

--------------------------------------------------------------

Update 11Jan2026: Chart 169:

MSCI EM Index - China and India weights: Quarterly changes between Dec2024 and Dec2025: (for old data, see old blogs dated 07Jan2023 and blog 03Aug2021 and previous charts below)

India's position in the MSCI EM Index continues

to be in third rank, as India has been underperforming grossly since

the beginning of 2025. China and Taiwan continue to dominate the index

as of 31Dec2025.

Overview of MSCI EM Index (as of 31Dec2025)

The MSCI Emerging Markets Index remains broad-based with 24 countries and just under 1,200 securities. Market capitalisation has risen sharply to about USD 10.2 trillion, reflecting both price appreciation and currency effects versus 2024 and early 2025.

Valuations have moved higher but are still moderate by historical EM standards.

Index Size and Breadth

The number of countries has been stable at 24 across all periods shown. The number of securities declined from 1,252 at end-2024 to 1,197 by end-2025, suggesting ongoing consolidation, delistings or stricter inclusion criteria.

Market Capitalisation Trend

Market cap increased from USD 7.7 trillion at end-2024 to USD 10.2 trillion by end-2025. This is a strong recovery and expansion phase for EM equities.

After a gap of four years, MSCI EM index outperformed MSCI World index in calendar year 2025 -- with MSCI EM index delivering 30.6 per cent return versus 19.5 per cent for MSCI World.

Valuation Metrics and Income

Forward P/E ratio rose from 11.9 at end-2024 to 13.5 by end-2025. Price-to-book increased from 1.8 to 2.2 over the same period.

These moves show clear valuation re-rating, though EM valuations remain below developed-market levels. Dividend yield has declined from about 2.6 percent to 2.3 percent, reflecting higher prices rather than weaker dividends.

Country Weights: Concentration and Shifts

China remains the dominant country but its weight fell to 27.6 per cent from peaks above 31 percent earlier in 2025. Taiwan’s weight increased to 20.6 per cent, reflecting strength in semiconductors.

India stands at 15.3 per cent, lower than its Dec2024 peak, but still structurally higher than in prior years.

South Korea's share increased to around 13 per cent, led by technoogy companies. Brazil continues to be the largest Latin American exposure at just over 4 per cent.

Overall, the top three countries account for more than 60 percent of the index, highlighting concentration risk.

Company Weights: Technology Dominance

TSMC is the single most important constituent at nearly 12 per cent, significantly higher than a year earlier. Tencent remains the second-largest holding at just under 5 per cent. Samsung, Alibaba and SK Hynix round out the top five.

Technology and related hardware dominate the index leadership, reinforcing the EM index’s sensitivity to the global semiconductor and China tech cycles.

India has only two companies in top 10, namely, HDFC Bank (rank 6th) and Reliance Industries ( rank 7th).

Key Implications for Investors

The index shows a clear valuation re-rating in 2025 alongside strong market cap growth, led by large-cap technology and North Asian markets.

Concentration risk remains high, particularly in TSMC and China–Taiwan exposure. Dividend income is becoming less attractive as prices rise.

Overall, EM appears to be in a cyclical upswing rather than a deep value phase, with returns increasingly dependent on earnings delivery and global tech demand rather than multiple expansion alone.

Click on the chart to view better >

--------------------------------------------------------------

Update 10Jan2026: Charts 166 to 168:

Major Foreign Holders of US Treasury Securities:

Three charts here are:

1. Top 20 Countries Holding US Treasuries:

2. India's Holdings of US Treasury Securities:

3. Comparing RBI holdings of US Treasuries, Foreign Currency Assets and Gold: Diversification Strategy of RBI Forex Reserves:

According

to the data published by the US Treasury, the total holdings of US

Treasury Securities held by all foreign residents are USD 9,243 billion

as at the end of Oct2025.

There

is an increase of USD 549 billion or 6.3 per cent, of US Treasury

holdings by foreign entities, versus a year ago. See Chart 1 below.

Japan

continues to be the biggest holder of US treasuries with holdings of

USD 1,200 billion, followed by the UK (878), China (689), Belgium (469) and Canada (419). The share of these top five countries in total

holdings are 13, 9.5, 7.5, 5.1 and 4.5 per cent respectively as at the end of Oct2025.

US Treasury Securities held by Foreign Residents:

As

of Oct2025, the US Treasury Securities held by Foreign Residents are

USD 9,243 billion. Of these, USD 3,880 billion are held by Foreign

Official sources and the remaining USD 5,363 billion are held by foreign

private entities.

Foreign Official Holdings: This

includes the holdings of foreign governments, central banks (like the

BoE, BoJ, PBOC, RBI) and other official institutions (like sovereign

wealth funds).

Foreign Private Holdings: This includes all other foreign investors. This is a very diverse group and includes:

Foreign commercial banks,

Foreign corporations,

Foreign pension funds and insurance companies,

Individual foreign investors, and

Other private entities and investment funds.

India holdings of US Treasury Securities:

As of Oct2025, India's holdings are USD 190.7 billion, compared to USD

241.4 billion as of Oct2024, a year on year fall of nearly 21 per cent. Indeed, this is a steep fall.

Of the total foreign holdings of US

Treasuries of USD 9,243 billion, India's share is 2.1 per cent now

compared to 2.8 per cent a year ago. Even in percentage terms, India's share has fallen significantly.

It may be noted India's central bank, RBI, holds offficial forex reserves on behalf of Government of India.

Proper perspective on India's UST holdings:

Past one year data on US Treasury holdings by India have been volatile. Recent peak for India's holdings of US Treasurys was USD 247.2 billion as at end of Sep2024.

From USD 241 bn in Oct2024, the holdings fell to USD 219 bn by Dec2024, but rose to USD 240 bn by Mar2025. In Apr2025, the holdings fell but rose in May2025, but declined again in Jun2025.

So, there is no clear pattern of selling or buying (here, we've not analysed the movement in the underlying dollar values of US Treasuries, which have seen dramatic volatility in recent years).

From Jun2025, the decline is sharp, with holdings falling every month till Oct2025. The holdings fell from USD 227 bn in Jun2025 to USD 191 bn in Octe2025.

We'are only analysing data of US Treasuries. We

don't know what the RBI holdings in sovereign bonds of other countries

are. For example, does RBI hold any sovereign bonds from the UK, France,

China, Brazil, Japan, South Africa or Nigeria for that matter?

One

needs to analyse the data dispassionately. It seems Indian media come

to the conclusion first and then present the data to suit their

conclusions, without considering the long term data or other connected

areas.

A corporate media yesterday published an article saying "India's UST holdings down by 21%, first time in four years." While this data point is correct, they fail to give a proper perspective to the sharp fall in holdings.

Media focus on recent quarters might exaggerate concern by not acknowledging the volatile holdings in the past one year.

In this context, we need to ask three basic questions?

One is why are India's UST holdings falling. Number two is whether the holdings of Treasuries of other countries are falling. And the third is whether the share of UST is falling in relation to India's foreign currency assets (FCA).

We don't know the answers to the first two questions because the RBI does not give any data on this. We can only speculate on the reasons. But we can definitely provide some context.

The proper context: Let us take the period of recent sharp fall in UST holdings, that is, between Jun2025 and Oct2025.

Between end-Jun2025 and end-Oct2025, India's UST holdings fell from USD 227.4 bn to USD 190.7 bn, a fall of USD 36.7 bn. How does the fall compare with India's FCA?

Between end-Jun2025 and end-Oct2025, India's foreign currency assets (FCA) fell by USD 30.2 bn from USD 594.8 bn to USD 564.6 bn. The share of UST in FCA fell form 38.2 per cent to 33.8 per cent (chart 3 below).

Why have FCA fallen? Because RBI has been selling dollars in the past four months.

How much dollars RBI has sold in four months upto Oct2025? It's a staggering USD 30 billion. This matches with the decline in UST holdings of RBI in the same period.

By the way, why is RBI selling dollars? Because RBI is defending the rupee (from falling too much) by selling dollars from its holdings of FCA.

When you want to sell your assets, which assets will you sell the most? In general, you will sell securities / assets that are most liquid.

This is exactly what RBI has been doing. They have been selling US dollar assets to defend the weakening Indian rupee. Because US Treaury securities are the most liquid assets in the world.

So,

India's central bank, the Reserve Bank of India, has no choice but to

sell the most liquid securities in its holdings, that is, the US

Treasuries.

The entire focus is on forex reserves, not on foreign currency assets (in the same period, forex reserves were up from USD 668 bn to USD 690 bn, due to rise in gold holdings driven by surging gold prices internationally).

(Note: The correct metric to use here is not forex reserves, but foreign

currency assets (FCA). India's forex reserves consist of foriegn currency

assets, gold holding and SDRs or special drawing rights.)

Now, let us come to the third question: How do you compare UST holdings to India's forign currency assets?

As mentioned above, the correct metric to use here is not forex reserves, but foreign

currency assets (FCA).

India's forex reserves are increasingly dominated by gold, hence let us use the FCA metric to compare with India's UST holdings (chart 3 below).

From Mar2022 to Oct2025, UST holdings declined from USD 199.8 billion to 190.7 billion,

while the their share in FCA declined significantly from

37 per cent to 33.8 per cent in the same period. But the UST holdings' share has been volatile in the past five years (chart 3 below).

This isn’t a divestment in absolute terms (holdings remain high), but a relative decline due to:

Gold price surge

Broader reserve accumulation

Possible currency diversification

Essentially, you need to link the fall in RBI's US Treasury holdings to the decline in the RBI’s foreign currency assets (FCA) and the quantity of net US dollar sales from forex intervention.

Without connecting these dots, the macro picture remains incomplete. 😃

Bonus data point: India's foreign currency assets (FCA) have

fallen between Mar2025 and Oct2025 from USD 567.6 billion to USD 564.6

billion. Nobody will tell you that. 😀

Diversification strategy of forex reserves by RBI:

Of course, the Reserve Bank of India (RBI) has been diversifying its forex reserves

in recent years. This is more pronounced since the outbreak of

Russia-Ukraine war in Feb2022. Since the outbreak of Russia-Ukraine

war, RBI holdings of US Treasury Securities have fallen from USD 200 bn to USD 191 bn now.

The value of RBI gold

holdings (due to a combination of sharp rise in dollar gold price

internationally and new physical gold bought by RBI) has increased over

the years and the share of gold reserves in total forex reserves too

has risen.

Significantly,

RBI has not practically bought any physical gold between Mar2025 and Oct2025. Its gold holdings remained stagnant at 880 metric tonnes in the

current financial year (chart 3 below).

However,

the market value of its gold holdings increased from USD 78.2 billion

in Mar2025 to USD 101.7 billion by Oct2025, as the gold has been reaching

all time highs recently (chart 3 below).

The share of market value of gold reserves in forex reserves has

increased steadily between Mar2020 (6.4%) and Oct2025 (14.8%), with value

increasing from USD 30.6 billion (physical gold hlding 653 million tonnes) to USD 101.7 billion (880 mt) -- but the increase is more pronounced since the start

of Russia-Ukraine war.

The value and share of gold holdings are climbing more rapidly, while the share of UST has declined sharply.

This reflects:

Price appreciation of gold (more than 75% rise in three years).

Buying of more physical gold by RBI over the years.

RBI's strategic allocation away from dollar-based assets.

Geopolitical risk hedging by RBI post-Russia-Ukraine war.

data sources:

Table 3: US Treasury Securities held by Foreign Residents

Three charts >

--------------------------------------------------------------

Update 03Jan2026: Charts 164 and 165:

Global market data: Global market data pertaining to stocks, bonds,

commodities and currencies are presented here. The data points are yearly changes and compounded returns from 2015 to 2025, indicating how the values have moved over the years. (old blog dated 12Jan2024 - global market data 2013 to 2023).

(See Update 04Jan2025 with charts 47 to 49)

The

stock market data presented in the table are price returns (not

including dividends) and they are in local currency terms.

Two charts here:

> Global market data: Yearly changes from 2015 to 2025

> Global market data: Compounded annual returns for 3-year, 5-y, 7-y and 10-y periods as at the end of 31Dec2025

You

can find out how the assets classes and currencies have moved over the

years. These charts reveal the cyclical nature of the returns in global

financial markets.

GLOBAL SNAPSHOT 2015–2025

All the analysis is as of 31Dec2025.

The two exhibits together show a decade that splits cleanly into three regimes: a pre-2020 expansion, a 2020–22 shock-and-whipsaw period, and a post-2022 normalisation with higher inflation and rates.

Returns are far more uneven than the headline averages suggest, with the US and India compounding strongly, Europe middling, and China/Hong Kong lagging badly. Volatility, not just growth, is the defining feature of the period.

EQUITIES: WHO WON THE DECADE

US equities dominate on compounding power. The Nasdaq is the standout on every horizon, reflecting the sustained outperformance of growth and technology sectors; the S&P 500 is a strong second.

India is the other clear winner: Nifty 50 and especially BSE MidCap show decent multi-year compounded returns (CAGR), pointing to a long domestic growth cycle plus multiple expansion.

Europe (FTSE 100, DAX 40) delivers modest long-term returns with sharp drawdowns, while Japan does better than Europe but still trails the US and India.

China and Hong Kong are the big laggards: despite occasional strong single years, their 5- to 10-year CAGRs are low to weak, indicating structural and policy headwinds overpowering cyclical rebounds.

EQUITIES: PATH MATTERS MORE THAN AVERAGES

The yearly change chart shows violent reversals: deep equity losses clustered in 2018, 2020 (select markets), and especially 2022, followed by sharp rebounds in 2023–25.

Markets with strong long-term CAGRs (Nasdaq, India MidCaps) also endured some of the worst single-year drawdowns, underscoring that endurance, not timing, drove success.

BONDS AND RATES: THE LOST DECADE FOR DURATION

Bond yields tell a clear story: the long downward trend ended decisively. Over 3-, 5-, 7- and 10-year horizons, the US Treasuries show large upward moves in yields, meaning negative price returns for long-duration bonds.

The worst damage is concentrated in the 2021–22 inflation shock, with only partial relief afterward.

The US Bonds failed as a volatility hedge in this cycle, breaking a key assumption of the prior decade.

India bonds too suffered during the inflation shock period of 2021 and 2022, but recovered later (When bond yields rise, bond prices drop and vice versa).

While US 10-year Treasury note yield rose by 271 basis points (1 percentage point equals 100 basis points); the India 10-year benchmark yield declined by 117 basis points in the past 10 years -- indicating divergent trends.

COMMODITIES: REAL ASSETS REASSERT THEMSELVES

Gold and silver show strong long-term CAGRs, reflecting inflation hedging, currency debasement fears and crisis demand. Energy is far more cyclical: crude oil has poor 3-year CAGR but acceptable 10-year returns, illustrating boom-bust dynamics rather than steady compounding.

Broad commodity indices sit in the middle, benefiting from the post-pandemic inflation burst but lacking the sustained momentum of precious metals.

BITCOIN: EXTREME RETURNS, EXTREME PATH

Bitcoin’s long-term CAGR dwarfs every other asset, but the yearly data reveal repeated crashes of 60–70 per cent plus. The message is binary: extraordinary wealth creation for holders who survived multiple near-death drawdowns, and total unsuitability for investors needing stability or predictable income.

It behaves more like a high-volatility venture asset than a currency or commodity.

CURRENCIES: DOLLAR STRENGTH AS A GRAVITY FORCE

Currency CAGRs are small compared to equities and commodities, but the pattern is consistent: the US dollar index trends stronger over most horizons, pressuring EUR and GBP.

INR depreciation is gradual and steady rather than chaotic, while JPY weakness stands out as a structural shift tied to policy divergence. Currency moves quietly but meaningfully shape real returns for global investors.

REGIONAL ROTATION AND CAPITAL FLOWS

Capital clearly favored innovation-heavy, rule-stable markets (the US) and high-growth domestic stories (India). Regions with regulatory uncertainty, demographic drag or geopolitical stress (China/Hong Kong, parts of Europe) saw capital leakage despite occasional rallies.

The data reflect not just economics, but trust, policy credibility and narrative.

PORTFOLIO IMPLICATIONS FROM THE DECADE

Diversification across assets mattered more than diversification within equities. Equities alone delivered uneven outcomes; bonds failed when inflation surged; real assets and gold provided balance; and a small allocation to extreme-growth assets dramatically altered outcomes.

The decade rewards long-term discipline, tolerance for volatility and exposure to structural growth rather than mean reversion bets.

BOTTOM LINE

2015–2025 was not a “smooth CAGR decade” but a stress test of conviction. The winners (like the so-called Magnificent 7 stocks) combined growth, policy credibility and innovation; the losers suffered from structural headwinds despite occasional strong years.

The next cycle will likely look different, but the lesson endures: compounding comes from staying invested in diversified assets with emphasis on proper asset allocation, not from wild speculation or asset / sector rotation.

--------------------------------------------------------------

Update 03Jan2026: Charts 162 and 163:

Dollar Rupee exchange rate: USD INR Exchange Rate: Calendar year-wise and financial year-wise data of the US dollar-Indian rupee exchange rate for the past 27 years (previous blog dated 03Jun2024 on Why RBI Won't Favour a Strong Rupee and preivous blog dated 01Jun2024 on how to calculate currency depreciation and appreciation) >

USD-INR yearly gain / loss

Exchange rate yearly gain / loss

Dollar rupee yearly gain / loss

USD-INR financial-year and calendar-year end data

USD-INR change %: Calendar year-wise: Dollar gain versus Rupee: Data include not only year-wise changes but also 5-year change

(annualised). For example, between end-Dec2016 and end-Dec2021, the

annualised appreciation for USD vs INR is only 1.8 per cent; whereas

between end-Dec2007 and end-Dec2012, it was 6.8 per cent annualised.

For the past 25 years, the USD has appreciated versus INR at an annualised rate of 2.65 per cent. Conversely, the Indian rupee depreciated against the US dollar at an annualised rate of 2.58 per cent.

Data range for CY-wise yearly change

for the past 27 years is: minus 1o.9 per cent to plus 22.9 per cent.

The data range is so wide one can't even predict / forecast the yearly

changes in USD-INR exchange rate.

Of

the 27 calendar years for which data are presented here, Govt of India

and Reserve Bank of India allowed the rupee to appreciate against the

dollar only on eight occasions.

INR-USD change %: (extreme right column in the table below): Column 6 shows how much the rupee has depreciated versus the dollar.

Financial year-wise: Dollar gain versus Rupee: Data include not only year-wise changes but

also 5-year change (annualised). For example, between end-Mar2020 and

end-Mar2025, the USD appreciated by 2.6 per cent annualised rate. And

between end-Mar2011 and end-Mar2016, the annualised USD appreciation vs

INR was much higher at 8.2 per cent.

For the past 25 years, USD has appreciated by an annualised 2.73 per cent versus INR.

Data range for FY-wise yearly change

for the past 26 years is: minus 11.4 per cent to plus 27.5 per cent.

The data range is so wide one can't even predict / forecast the yearly

changes in USD-INR exchange rate.

Of

the 26 financial years for which data are presented here, Govt of India

and Reserve Bank of India allowed the rupee to appreciate against the

dollar only on eight occasions.

Data for USD–INR are from RBI DBIE. All other calculations are by the author.

Explanation for two columns in the two tables presented below >

Column 3 (USD–INR change %): This shows how much the value of one US dollar changed compared to the Indian rupee during the year. A positive number means the dollar became stronger (it took more rupees to buy one dollar). A negative number shows the dollar depreciation versus rupee (dollar became weaker).

Column 6 / extreme right (INR–USD change %): This shows how much the value of one Indian rupee changed compared to the US dollar during the year. A positive number shows the rupee appreciation (one rupee could buy more dollars). A negative number means the rupee became weaker versus the dollar.

--------------------------------------------------------------

Update 02Jan2026: Charts 156 to 161:

FPI Equity Flows to India: India

FPI Flows to Indian stock market and debt market in rupee terms > (old blog 10Jul2022) >

In calendar year 2025, FPI equity flows were negative in eight months. Despite a lot of negatives, Nifty 50 managed a positive return of 10 per cent in CY 2025.