Analysis of Small Savings Schemes and Interest Rates

(This

is for information purposes only. This should not be construed as a

recommendation or investment advice even though the author is a CFA Charterholder. Please consult your financial

adviser before taking any investment decision. Safe to assume the author has a vested

interest in stocks / investments discussed if any.)

Small savings schemes are popular financial products. These schemes are available through Government of India's Post Office and various banks. They provide highest safety of principal and interest, as they are fully guaranteed by the government, irrespective of the amount.

1. What are these schemes?

Some of the popular schemes are Post Office term deposits offered for one-, two-, three- and five-year periods, Post Office Monthly Income Scheme (POMIS), Public Provident Fund (PPF), Senior Citizens Savings Scheme (SCSS) and five-year National Savings Certificate (NSC).

The popularity of the schemes can be gauged from the amount outstanding against each scheme given in table 1 below. Savers are obviously attracted toward schemes, such as, Post Office term deposits accounts, POMIS, Post Office savings bank accounts and Kisan Vikas Patra or KVP.

Table 1: Small savings schemes and outstandings:

As shown in table 1 above, the

total outstanding of these schemes is Rs 15.77 lakh crore as at the end

of December 2022, until which latest data is available. Table 1 provides data beloning to individual schemes as at the end of March 2022.

Traditionally, small savings schemes have enjoyed income tax concessions and as such they have become default financial savings for all kinds of savers.

In recent years, tax concession has been extended to bank deposits. Bank deposits also enjoy deposit insurance, in insured banks, of up to Rs 5 lakh per depositor.

In the past six to seven years, mutual funds too have attracted the attention of savers. Debt mutual funds too have become popular with investors.

(blog continues below)

------------------------------Related blogs:

Small Savings Interest Rates 04Mar2014

Understanding Floating Rate Savings Bonds 2020 (Taxable) 05May2023 - FRSB

Negative Impact of Debt Mutual Fund Tax Changes 25Mar2023

How Rates and Ratios are Moving 26May2022

Saver's curse: Low Savings Rates and Liquid Mutual Fund Returns 10Dec2021

------------------------------

2. Rise of popularity recently

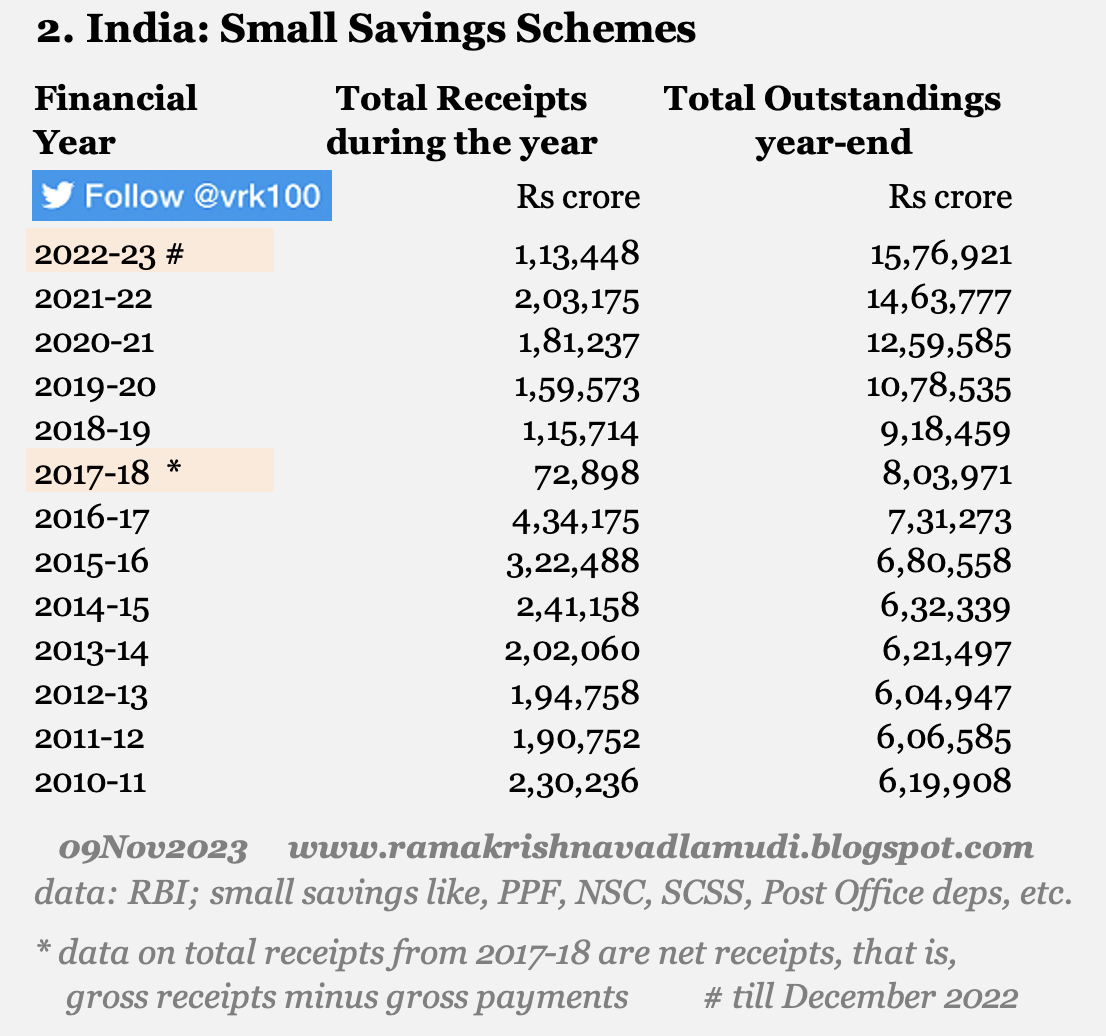

Between March 2018 and March 2022, the total outstandings rose from Rs 8.04 lakh crore to Rs 14.64 lakh crore, an annualised growth of 16 percent. The total outstandings further grew to Rs 15.77 lakh crore by the end of December 2022.

It could be said the total outstandings have doubled in the past five years.

Total receipts grew from Rs 73,000 crore in 2017-18 to Rs 203,000 crore in 2021-22, clocking an annualised growth of 29 percent, clearly indicating the rise in popularity of these schemes.

Table 2: Total receipts and outstanding amounts: (data of total receipts from FY 2017-18 are net receipts, that is, gross receipts minus gross payments)

Some of reasons for their increased popularity could be:

-- after the note ban (demonetisation) of November 2016, bank interest rates fell to as low as 6 to 7 percent attracting several investors to small savings schemes offering higher rates

-- investors who invested debt mutual funds lost heavily in 2020 (Franklin Templeton debt fiasco) and they took shelter under the safety of small savings schemes

-- collapse of Infrastructure Leasing and Financial Services (IL&FS), a non-bank financial company (NBFC) in 2018 negatively impacted several other NBFCs and the contagion spread to various other financial players -- investors looking for alternatives found small savings schemes more attractive

3. Small Savings Interest Rates

Even how interest rates are calculated is changed arbitrarily.

For example, effective 01Apr2016, the Government arbitrarily changed the half-yearly compounding to yearly compounding

on NSC, whereby investors would be losing 20 to 25 basis

points of interest every year--amounting to substantial loss in five

years (NSC - National Savings Certificates).

Table 3: Interest rates on small savings: (please click on the image to view better)

As highlighted in table 3 above, effective 1st of April 202o, interest rates were cut drastically impacting millions of senior citizens and other small investors.

For example, Post Office one-year term deposit rate was slashed from 6.9 to 5.5 percent per year. Interest on SCSS was cut from 8.6 to 7.4 percent and that of 5-year NSC from 7.9 to 6.8 percent.

PPF savers under the bus:

It may be noted in March 2020, India like other nations imposed draconian lockdown due to outbreak of COVID-19 Pandemic. Indians reeled not only under the Pandemic but also suffered due to lower interest rates in times of elevated inflation.

Ever since April 2020, PPF interest has been kept at 7.10 percent without any logic.

Employee Provident Fund (EPF) scheme enjoys an interest rate of more than 8 percent for several decades. Interestingly, this rate is not market-determined.

But small savings schemes are supposed to be market-determined (in practice, they are not).

But small savings schemes are supposed to be market-determined (in practice, they are not).

Nobody is demanding higher rates to small savings at the cost of exchequer. From a long term viewpoint, all interest rates should be determined as per market rates. The government does not lose much if the PPF interest rates as per their own policy of market-determined interest rates.

But as India does not have any social security benefits, it is better if the government continues to provide interest rates a little higher (say, one percentage point higher) than the market rates.

New tax regime discourages savings:

With two tax regimes, India has more than 13 or 14 tax slabs to deal with, which is almost a world record of sorts! Under the new tax regime, individuals can pay lower income tax, but they have to forego tax concessions offered by the government.

In a country with no social security, it is not clear how people will be able to manage their money matters without any tax reliefs and attractive retirement products.

It seems to be the objective of the government to discourage savings in India by

removing tax incentives for various savings schemes and other items in

the new tax regime.

4. Summary

A plethora of financial products are available to savers who need the benefits of safety, convenience and liquidity. While small savings schemes provide highest safety and tax concessions, most of the schemes are not liquid -- meaning they cannot be converted into cash easily and quickly.

It would be better if the government provides online investment facility to some small savings schemes, like, NSC.

Not all fixed income products are suitable to investors.

Small savings schemes, bank deposits and debt mutual funds

offer investors various degress of safety, convenience, liquidity and taxability. Based on their investment goals, invetors can choose from a bouquet of products.

- - -

------------------------------

References:

RBI Handbook of Statistics on Indian Economy (HBIE) - tables 114 and 115 provide data on small savings interest rates, yearly total receipts and yearly outstandings

RBI monthly bulletin - table 44 provides data on small savings as Occasional Series (only some monthly bulletins contain this data)

Notes on Tables of RBI's HBIE (these notes on table 114 provide changes to various small savings schemes over the years)

MoF DEA small savings interest rates

Tweet 17Dec2019 India Gazette notification - Several old acts (like PPF Act 1968, NSC Act, etc.) were subsumed into Government Savings Promotion Act, 1873 and these new rules are now notified as per this GSP Act of 1873

-- above notification web archive

PPF interest rate history from RBI...

EPF interest rate history from EPFO....

How Rates and Ratios are Moving

Negative Impact of Debt Mutual Fund Tax Changes

The Scourge of Negative Real Interest Rates Continues

Tweet 16Feb2016 on market-determined small savings rates

Tweet 26Sep2018 on small savings schemes

The June2011 Report of the Shyamala Gopinath Commitee on Comprehensive Review of NSSF -- Govt decisions dt 11Nov2011 on the Committee's recos

------------------------------

Read more:

Blog of Blogs Theme-wise

Is De-Dollarization Real?

India Debuts 50-year Sovereign Bond

India: Prospects and Challenges

India Public Debt and Floating Rate Bonds

India Equity ETFs Worth Considering

JP Morgan Guide to Markets Sep2023

Mutual Fund Asset Class Returns 30Sep2023

Divergence in Volatile Global Bond Yields

Global Market Data 30Sep2023

India's Crude Oil Import Dependency Jumps under Modi

Analysis of Nifty 100 Low Volatility 100 Index

Short Opinion on HDFC Bank

Buyback Offers and Weblinks

Understanding Floating Rate Savings Bonds 2020 (Taxable)

Negative Impact of Debt Mutual Fund Tax Changes

Weblinks and Investing

-------------------

Disclosure: I've vested interested in Indian stocks and other investments. It's safe to assume I've interest in the financial instruments / products discussed, if any.

Disclaimer: The analysis and opinion provided here are only for information purposes and should not be construed as investment advice. Investors should consult their own financial advisers before making any investments. The author is a CFA Charterholder with a vested interest in financial markets.

CFA Charter credentials - CFA Member Profile

CFA Badge

He blogs at:

https://ramakrishnavadlamudi.blogspot.com/

X (Twitter) @vrk100

No comments:

Post a Comment