Spectacular Rise of India's Retail Investors and Demat Accounts

(Tables giving details of updated information as on 31Mar2024, 31Dec2023, 30Sep2023, 31Mar2023 31Dec2022, 30Sep2022, 31Aug2022, 31May2022 and 31Mar2022 are added at the end of the article)

For long, retail investors' participation in Indian stock markets had been moderate. However, since 2014 there has been a steady rise in retail participation; and the growth trend has seen spectacular acceleration since 2020 after the outbreak of Corona Virus Pandemic.

Retail Participation and Demat Accounts

The participation is encapsulated in the number of new demat accounts opened and the growth of trading volumes by retail investors.

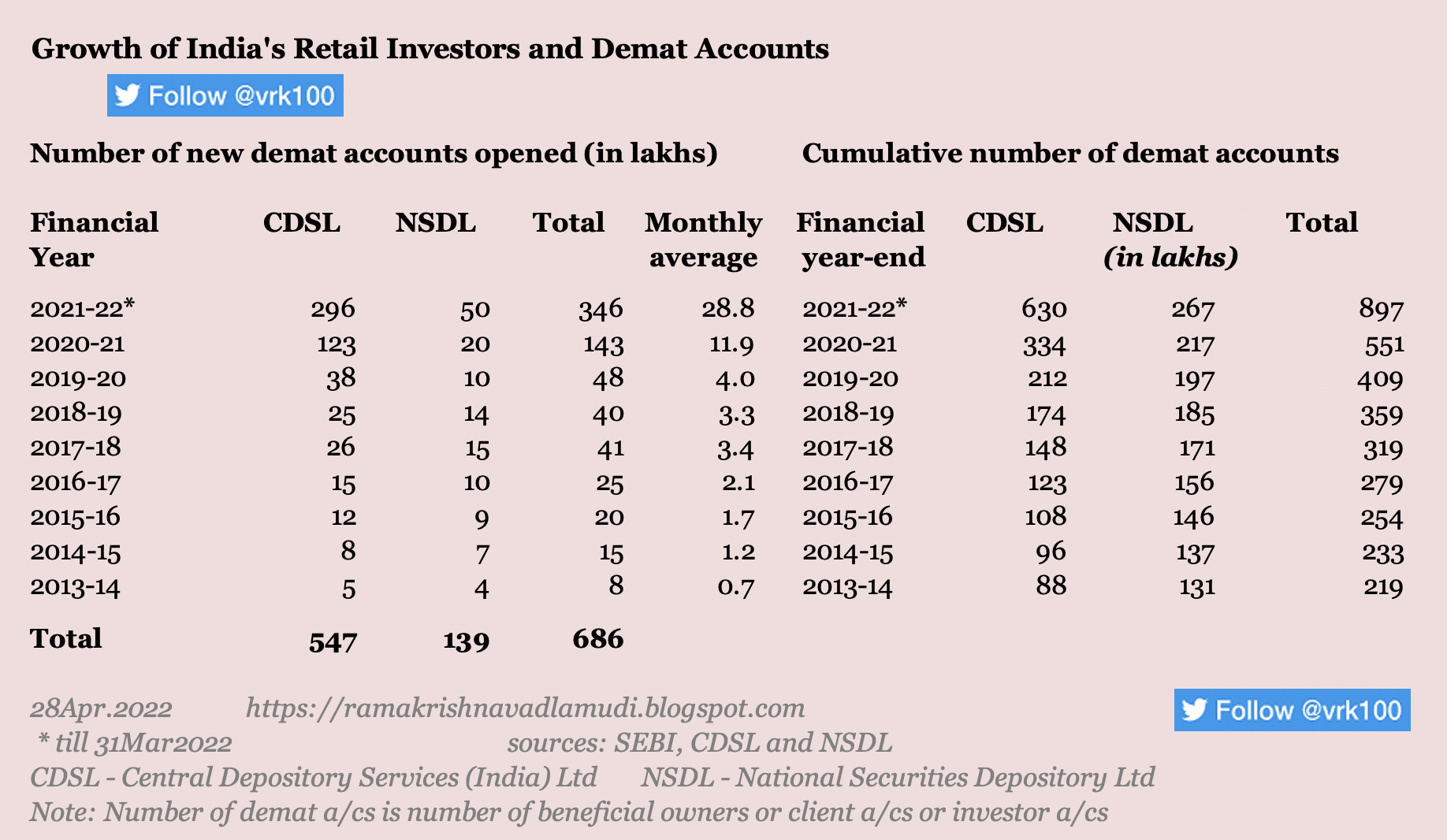

It is quite astonishing to note that the number of demat accounts opened in FY 2021-22 (from April 2021 till now) is more than the number of accounts opened in the previous five years (2016-17 to 2020-21)!

During FY 2014-15, the monthly average of number of new demat accounts opened used to be about 1.2 lakh and the monthly average surged to nearly 29 lakh accounts (average for the first ten months of FY 2021-22). (see Table 1 for details)

Due to the extraordinary rise in new demat accounts opened since April 2020, the cumulative number of demat accounts rose to 840 lakh as at the end of January 2022 from 409 lakh accounts (cumulative) in March 2020--a rise of more than 100 per cent in under two years period.

The numbers cited above include those from CDSL and NSDL, the two depositories in India.

Table 1: New Demat Accounts Opened and Cumulative Accounts>

One interesting sidelight is that CDSL's Market Share in the number of cumulative demat accounts grew from 40 per cent at the end of March 2014 to about 70 per cent as at the end of January 2022 (see Table 1 for data).

Obviously, this rise of CDSL's share has come at the cost of its only rival depository, that is, NSDL.

-------------------

Read more:

RBI Announces USD-INR Sell/Buy Swap Auction

ETF Compare - Nifty BeES and Junior BeES

BSE 500 vs S&P 500 Indices

Who is Eating my Gold ETF Return?

Foreign Investors Waning Interest in Indian Stocks

Indian Equity ETF Risks and Returns

Do Paint Stocks and Crude Oil Tango?

Weblinks and Investing-------------------

Retail Participation and Trading Volumes

As per Central Depository Services (India) Limited, the turnover of shares traded on BSE increased from Rs 5.2 lakh crore in FY 2013-14 to Rs 10.5 lakh crore in FY 2020-21; while the turnover on NSE rose from Rs 28.1 lakh crore to Rs 154 lakh crore in the same period.

BSE and NSE are two premier stock exchanges in India.

As per NSE Market Pulse (Jan2022 issue), individual investors' share in the capital market segment (cash segment) has been growing in recent years, whereas the share of domestic insitituional investors (DIIs) and foreign portfolio investors (FPIs) has been on the wane in the same period. The market share of individual investors increased from 33 per cent during FY 2015-16 to 45 per cent during FY 2020-21. The share has fallen to 41.6 per cent in FY 2021-22 (April 2021 to December 2021).

The Individual investors category includes individual domestic investors, non-resident Indians (NRIs), Hindu Undivided Families (HUFs) and sole proprietorship firms.

Indices Growth

As retail investors evince more interest in mid- and small-cap stocks rather than large-cap stocks, the relative growth of mid- and small-cap indices reflects their enthusiastic participation.

As delineated in Table 2, Nifty 50 index representing large-cap stocks rose by 142 per cent between March 2014 and today; whereas BSE Mid-cap and Small-cap indices showed a much higher growth of 214 and 259 per cent respectively in the same period.

As the history suggests, mid- and small-cap stocks entail higher risks as compared to large-cap stocks. The number of bankruptcies is higher in mid- and small-cap stocks and they exhibit higher volatility in times of economic and political uncertainty.

Despite the known risks, retail investors tend to dabble more in these groups of stocks.

Table 2: Indices growth >

To Sum Up

The growth of retail investors is a positive development for India's capital markets, as this increases the liquidity and breadth of markets. However, as the experiences in the Harshad Mehta Scam of 1992-94 and the 2001 Ketan Parekh Scam have shown, euphoria of retail investors may have negative consequences.

Of course, retail investors have been learning a lot of lessons from the market upheavals. The increased use of digital tools in markets may help new investors and enhance the maturity of markets.

Even as I'm writing this article, Russia has invaded Ukraine. This is likely to have dire consequences for citizens of Ukraine. Ukraine has been caught napping in the tussle between NATO (North Atlantic Treaty Organization) expansion, European and US political interests.

These are testing times for financial markets, nation(s) caught in the NATO-US-Europe crossfire and for geopolitics and globalisation in general.

It's also a test of retail investors' patience with markets. Let us see how they will respond to the latest turmoil.

- - -

P.S.: Data update on 08May2024 with data till 31Mar2024 > Total number of demat accounts, combined for CDSL and NSDL, as at close of 31Mar2024 reached 15.05 crore > CDSL market share in total number of a/cs further increased to 76.8 per cent >

monthly average of new demat a/cs opened was 30 lakh in the full FY 2023-24; which is much better than the FY 2022-23 monthly average of 20.7 lakh >

P.S.: Data update on 21Feb2024 with data till 31Dec2023 > Total number of demat accounts, combined for CDSL and NSDL, as at close of 31Dec2023 reached 13.93 crore > CDSL market share in total number of a/cs further increased to 75.2 per cent >

monthly average of new demat a/cs opened was 27.6 lakh in the first nine months of FY 2023-24; which is much better than the FY 2022-23 monthly average of 20.7 lakh >

P.S.: Data update on 23Oct2023 with data till 30Sep2023 > Total number of demat accounts, combined for CDSL and NSDL, as at close of 30Sep2023 reached 12.97 crore > CDSL market share in total number of a/cs increased to 74.2 per cent >

monthly average of new demat a/cs opened was 25.3 lakh in the first six months of FY 2023-24; which is much better than the FY 2022-23 monthly average of 20.7 lakh >

P.S.: Data update 31Mar2023 > Total number of demat accounts, combined for CDSL and NSDL, as at close of 31Mar2023 reached 11.45 crore > CDSL market share in total number of a/cs increased to 72.5 per cent >

monthly average of new demat a/cs opened was 28.8 lakh in FY 2021-22; this has slowed down to 20.7 lakh monthly average in FY 2022-23 (for 12 months) >

of the cumulative demat accounts of 11.45 crore as on 31Mar2023, 64.3 percent (or 7.36 crore) were opened in the past three financial years (between FY 2020-21 to 2022-23) > this is due to change in people's behaviour after COVID-19 Pandemic and the power and ease of technology (like, ease of mobile stock trading applications and payment apps) >

P.S.: Data update 31Dec2022 > Total number of demat accounts, combined for CDSL and NSDL, as at close of 31Dec2022 reached 10.83 crore > CDSL market share in total number of a/cs increased to 71.9 per cent >

monthly average of new demat a/cs opened was 28.8 lakh in FY 2021-22; this has slowed down to 20.6 lakh monthly average in FY 2022-23 (for 9 months) >

P.S.: Data update 30Sep2022 > Total number of demat accounts, combined for CDSL and NSDL, as at close of 30Sep2022 reached 10.26 crore > CDSL market share in total number of a/cs increased to 71.5 per cent >

P.S.: Data update 31Aug2022 > Total number of demat accounts, combined for CDSL and NSDL, as at close of 31Aug2022 reached 10 crore > CDSL market share in total number of a/cs increased to 71.3 per cent >

P.S.: Data update 31May2022

> Total number of demat accounts, combined for CDSL and NSDL, as at close of 31May2022 reached nearly 948 lakhs > CDSL market share in total number of a/cs increased to 70.9 per cent >

P.S.: Data update 31Mar2022 >Phenomenal rise in demat account by CDSL during FY 2021-22 whereas NSDL is lagging way behind > Seventy per cent of all demat accounts in India are from CDSL >

References:

NSE Market Pulse Jan2022 Issue >

CDSL Newletter - CDSL infoline

NSDL updates - data on demat a/cs, etc.

SEBI Bulletin Feb2022

Disclosure: I've vested interested in Indian stocks and other investments. It's safe to assume I've interest in the financial instruments / products discussed, if any.

Disclaimer: The analysis and opinion provided here are only for information purposes and should not be construed as investment advice. Investors should consult their own financial advisers before making any investments. The author is a CFA Charterholder with a vested interest in financial markets.

CFA Charter credentials - CFA Member Profile

CFA Badge

He blogs at:

https://ramakrishnavadlamudi.blogspot.com/

Twitter @vrk100

No comments:

Post a Comment